Given the following two time series (x, y; see below), what is the best method to model the relationship between the long-term trends in this data?

Both time series have significant Durbin-Watson tests when modelled as a function of time and neither are stationary (as I understand the term, or does this mean it only needs to be stationary in the residuals?). I have been told that this means I should take a first-order difference (at least, maybe even 2nd order) of each time series before I can model one as a function of the other, essentially utilising an arima(1,1,0), arima(1,2,0) etc.

I don't understand why you need to detrend before you can model them. I understand the need to model the auto-correlation, but I don't understand why there needs to be differencing. To me, it appears as though detrending by differencing is removing the primary signals (in this case the long-term trends) in the data that we are interested in and leaving the higher-frequency "noise" (using the term noise loosely). Indeed, in simulations where I create an almost perfect relationship between one time series and another, with no autocorrelation, differencing the time series gives me results that are counterintuitive for relationship detection purposes, e.g.,

a = 1:50 + rnorm(50, sd = 0.01)

b = a + rnorm(50, sd = 1)

da = diff(a); db = diff(b)

summary(lmx <- lm(db ~ da))

In this case, b is related strongly with a, but b has more noise. To me this shows that differencing doesn't work in an ideal case for detecting relationships between low frequency signals. I understand that differencing is commonly used for time-series analysis, but it appears to be more useful for determining relationships between high-frequency signals. What am I missing?

Example Data

df1 <- structure(list(

x = c(315.97, 316.91, 317.64, 318.45, 318.99, 319.62, 320.04, 321.38, 322.16, 323.04, 324.62, 325.68, 326.32, 327.45, 329.68, 330.18, 331.08, 332.05, 333.78, 335.41, 336.78, 338.68, 340.1, 341.44, 343.03, 344.58, 346.04, 347.39, 349.16, 351.56, 353.07, 354.35, 355.57, 356.38, 357.07, 358.82, 360.8, 362.59, 363.71, 366.65, 368.33, 369.52, 371.13, 373.22, 375.77, 377.49, 379.8, 381.9, 383.76, 385.59, 387.38, 389.78),

y = c(0.0192, -0.0748, 0.0459, 0.0324, 0.0234, -0.3019, -0.2328, -0.1455, -0.0984, -0.2144, -0.1301, -0.0606, -0.2004, -0.2411, 0.1414, -0.2861, -0.0585, -0.3563, 0.0864, -0.0531, 0.0404, 0.1376, 0.3219, -0.0043, 0.3318, -0.0469, -0.0293, 0.1188, 0.2504, 0.3737, 0.2484, 0.4909, 0.3983, 0.0914, 0.1794, 0.3451, 0.5944, 0.2226, 0.5222, 0.8181, 0.5535, 0.4732, 0.6645, 0.7716, 0.7514, 0.6639, 0.8704, 0.8102, 0.9005, 0.6849, 0.7256, 0.878),

ti = 1:52),

.Names = c("x", "y", "ti"), class = "data.frame", row.names = 110:161)

ddf<- data.frame(dy = diff(df1$y), dx = diff(df1$x))

ddf2<- data.frame(ddy = diff(ddf$dy), ddx = diff(ddf$dx))

ddf$ti<-1:length(ddf$dx); ddf2$year<-1:length(ddf2$ddx)

summary(lm0<-lm(y~x, data=df1)) #t = 15.0

summary(lm1<-lm(dy~dx, data=ddf)) #t = 2.6

summary(lm2<-lm(ddy~ddx, data=ddf2)) #t = 2.6

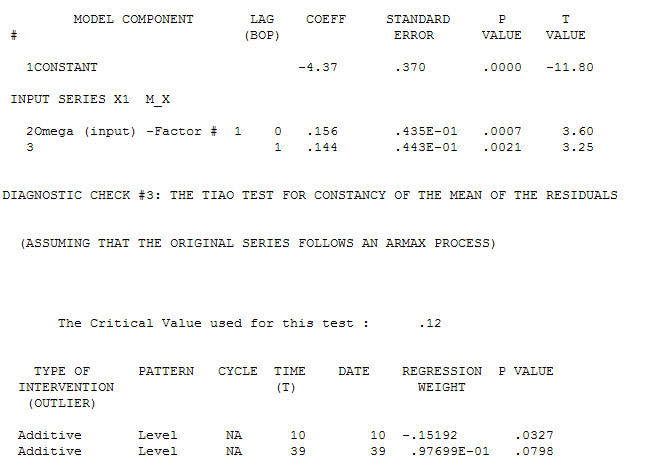

for your data yielding significant structure while rendering a Gaussian Error process

for your data yielding significant structure while rendering a Gaussian Error process  with an ACF of

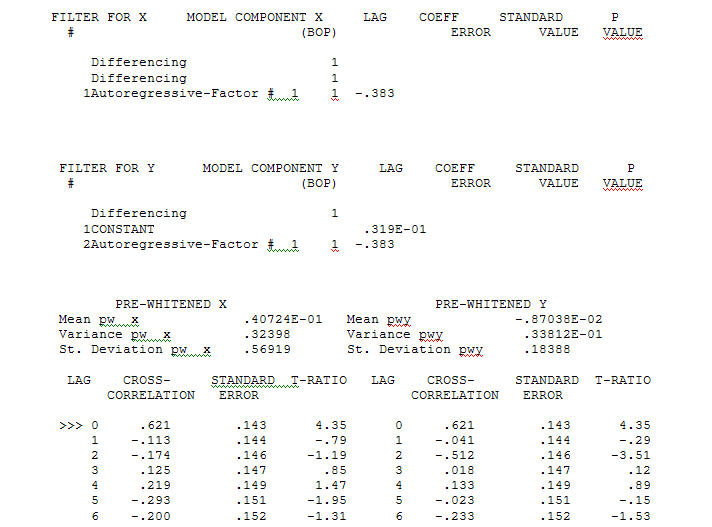

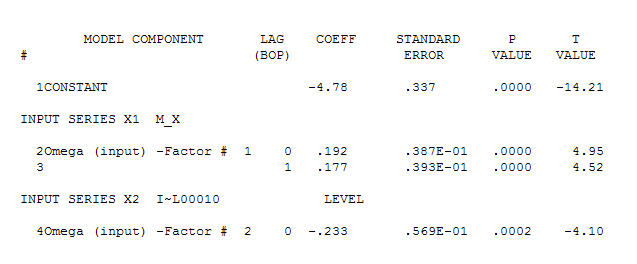

with an ACF of  the Transfer Function Identification modelling process requires ( in this case ) suitable differencing to create surrogate series that are stationary and thus usable to IDENTIFY the relationshop. In this the differencing requirements for IDENTIFICATION were double differencing for the X and single differencing for the Y. Additionally an ARIMA filter for the doubly differenced X was found to be an AR(1). Applying this ARIMA filter ( for identification purposes only ! ) to both stationary series yielded the following cross-correlative structure .

the Transfer Function Identification modelling process requires ( in this case ) suitable differencing to create surrogate series that are stationary and thus usable to IDENTIFY the relationshop. In this the differencing requirements for IDENTIFICATION were double differencing for the X and single differencing for the Y. Additionally an ARIMA filter for the doubly differenced X was found to be an AR(1). Applying this ARIMA filter ( for identification purposes only ! ) to both stationary series yielded the following cross-correlative structure . suggesting a simple contemporaneous relationship.

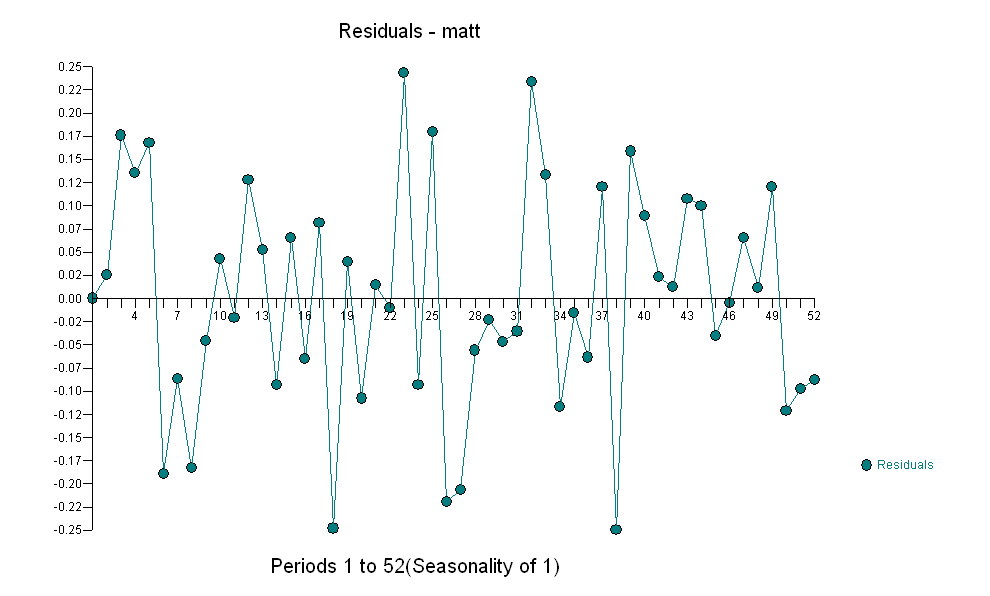

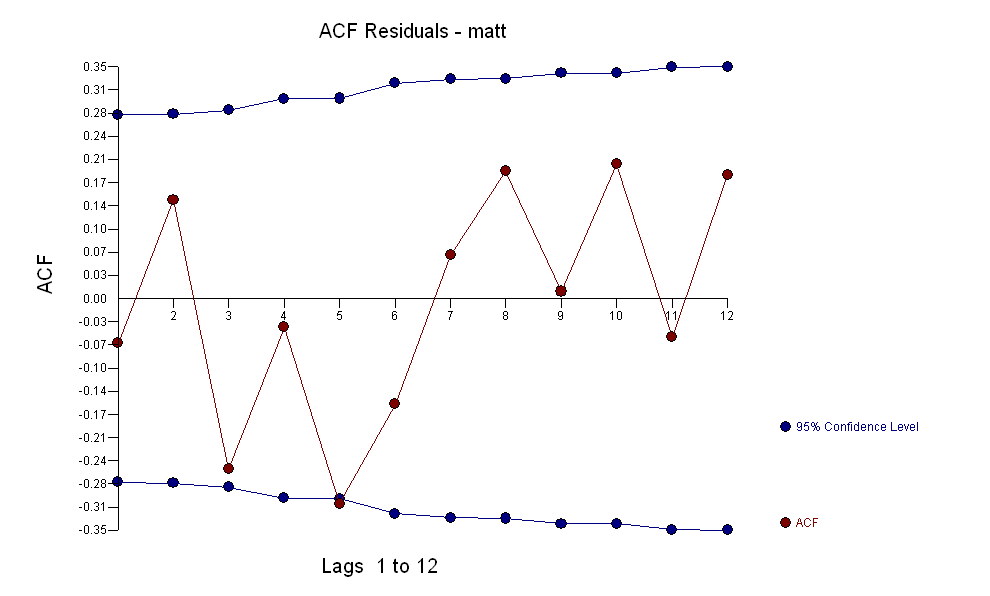

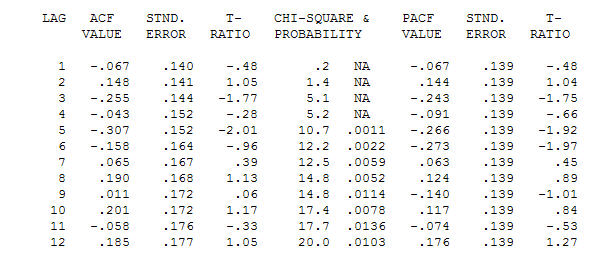

suggesting a simple contemporaneous relationship. . Note that while the original series exhibit non-stationarity this does not necessarily imply that differencing is needed in a causal model. The final model

. Note that while the original series exhibit non-stationarity this does not necessarily imply that differencing is needed in a causal model. The final model  and final acf support this

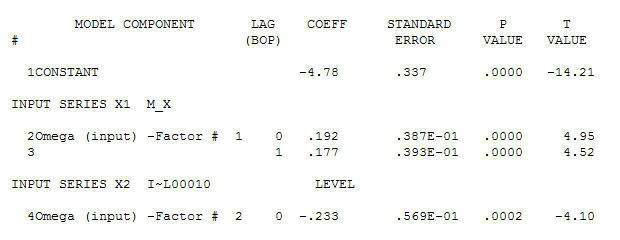

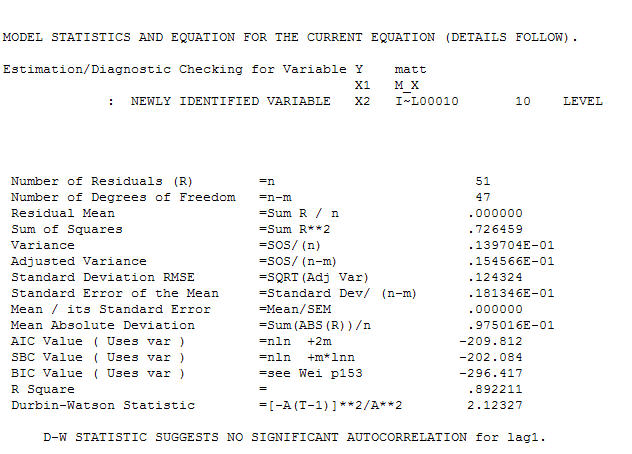

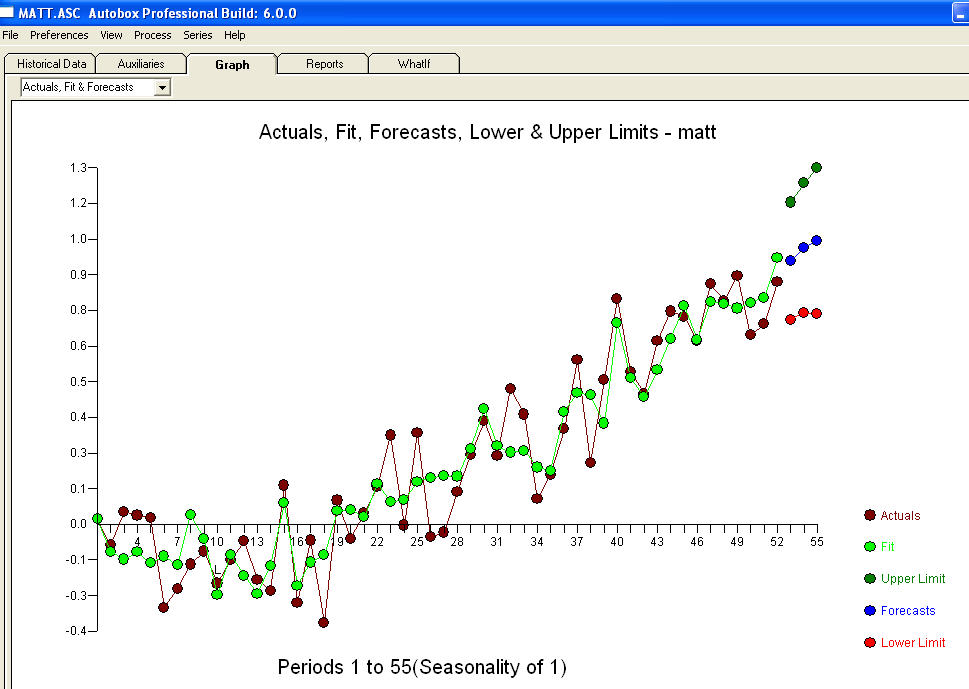

and final acf support this  . In closing the final equation aside from the one empirically identified level shifts ( really intercept changes ) is

. In closing the final equation aside from the one empirically identified level shifts ( really intercept changes ) is

. Statistics are like lampposts, some use them to lean on others use them for illumination.

. Statistics are like lampposts, some use them to lean on others use them for illumination.