Here are three (somewhat related) questions about the (Generalized) Method of Moments. I have only just today started studying this method.

- Concerning the following statement by Greene:

Why is $g$ not a function only of $Y_t$? My understanding was that $g$ should be computable from the sample, but if the true parameter (which is unknown) influences $g$, then we cannot compute it.

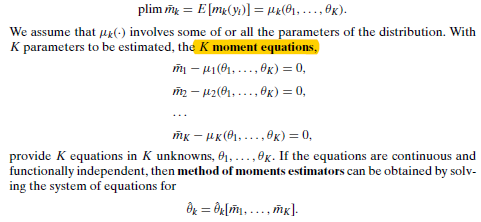

- Greene states that for the Methods of Moments estimator, we have $E(m_k(y_l))=\mu_k(\theta_1,...,\theta_k)$, where I understand $m_k(\cdot)$ to be the $k$'th sample-moment and $\mu_k$ the $k$'th population moment.

However, Greene then states that for the Generalized methods of moments estimator we need the "moment conditions":

perhaps these $m_{l,K}$ refer to something other than the moments, but I don't understand why this equation is different for the Generalized method, compared to the (non-generalized) method of moments. (Greene doesn't seem to explain this, if I'm not mistaken).

- This also partially justifies the following question: Is the "moment condition" synonymous with "moment equation"? Greene uses both words, without clearly defining a difference.