I understand that in many cases we difference time series. This is to make them stationary and stationary time series are good to have before forecasting (something about stabilizing the mean).

My question is, does percent change basically make a time series stationary?

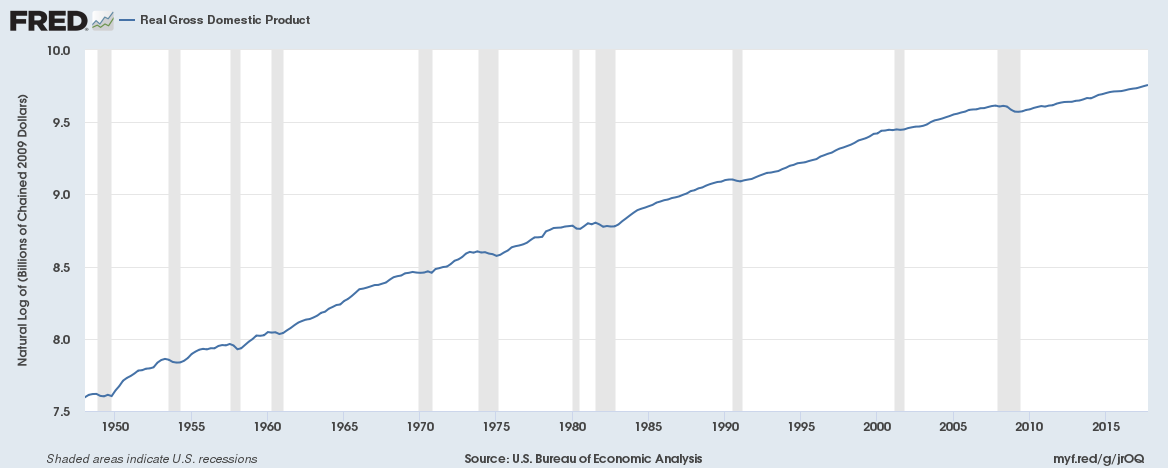

As a toy example, I think of gdp and percent change in gdp.

It seems to me the differencing takes the difference of the current period and the previous period. This is the "kernel" of the percent change formula. If I were to forecast gdp would I use percent change as the outcome, create my own difference off of gdp, or use gdp directly.

Also, as a secondary question, does differencing usually occur on the previous observation or could you difference this period this year vs this period last year. This is relevant to the above question because sometimes we don't want to know about percent change in relation to the previous observation, but to the same time last year.