You use the quantile regression estimator

$$\hat \beta(\tau) := \arg \min_{\theta \in \mathbb R^K} \sum_{i=1}^N \rho_\tau(y_i - \mathbf x_i^\top \theta).$$

where $\tau \in (0,1)$ is constant chosen according to which quantile needs to be estimated and the function $\rho_\tau(.)$ is defined as

$$\rho_\tau(r) = r(\tau - I(r<0)).$$

In order to see the purpose of the $\rho_\tau(.)$ consider first that it takes the residuals as arguments, when these are defined as $\epsilon_i =y_i - \mathbf x_i^\top \theta$. The sum in the minimization problem can therefore be rewritten as

$$\sum_{i=1}^N \rho_\tau(\epsilon_i) =\sum_{i=1}^N \tau \lvert \epsilon_i \lvert I[\epsilon_i \geq 0] + (1-\tau) \lvert \epsilon_i \lvert I[\epsilon_i < 0]$$

such that positive residuals associated with observation $y_i$ above the suggested quantile regression line $\mathbf x_i^\top \theta$ are given the weight of $\tau$ while negative residuals associated with observations $y_i$ below the suggested quantile regression line $\mathbf x_i^\top \theta$ are weighted with $(1-\tau)$.

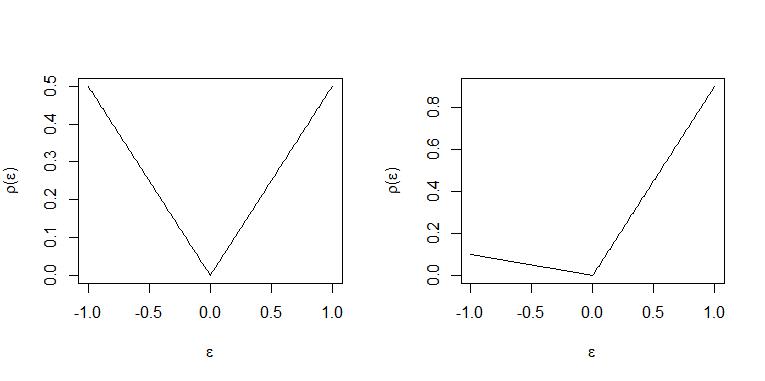

Intuitively:

With $\tau=0.5$ positive and negative residuals are "punished" with the same weight and an equal number of observation are above and below the "line" in optimum so the line $\mathbf x_i^\top \hat \beta$ is the median regression "line".

When $\tau=0.9$ each positive residual is weighted 9 times that of a negative residual with weight $1-\tau= 0.1$ and so in optimum for every observation above the "line" $\mathbf x_i^\top \hat \beta$ approximately 9 will be placed below the line. Hence the "line" represent the 0.9-quantile. (For an exact statement of this see THM. 2.2 and Corollary 2.1 in Koenker (2005) "Quantile Regression")

The two cases are illustrated in these plots. Left panel $\tau=0.5$ and right panel $\tau=0.9$.

Linear programs are predominantly analyzed and solved using the standard form

$$(1) \ \ \min_z \ \ c^\top z \ \ \mbox{subject to } A z = b , z \geq 0$$

To arrive at a linear program on standard form the first problem is that in such a program (1) all variables over which minimization is performed $z$ should be positive. To achieve this residuals are decomposed into positive and negative part using slack variables:

$$\epsilon_i = u_i - v_i$$

where positive part $u_i = \max(0,\epsilon_i) = \lvert \epsilon_i \lvert I[\epsilon_i \geq 0]$ and $v_i = \max(0,-\epsilon_i) =\lvert \epsilon_i \lvert I[\epsilon_i < 0]$ is the negative part. The sum of residuals assigned weights by the check function is then seen to be

$$\sum_{i=1}^N \rho_\tau(\epsilon_i) = \sum_{i=1}^N \tau u_i + (1-\tau) v_i = \tau \mathbf 1_N^\top u + (1-\tau)\mathbf 1_N^\top v,$$

where $u = (u_1,...,u_N)^\top$ and $v=(v_1,...,v_N)^\top$ and $\mathbf 1_N$ is vector $N \times 1$ all coordinates equal to $1$.

The residuals must satisfy the $N$ constraints that

$$y_i - \mathbf x_i^\top\theta = \epsilon_i = u_i - v_i$$

This results in the formulation as a linear program

$$\min_{\theta \in \mathbb R^K,u\in \mathbb R_+^N,v\in \mathbb R_+^N}\{ \tau \mathbf 1_N^\top u + (1-\tau)\mathbf 1_N^\top v\lvert y_i= \mathbf x_i\theta + u_i - v_i, i=1,...,N\},$$

as stated in Koenker (2005) "Quantile Regression" page 10 equation (1.20).

However it is noticeable that $\theta\in \mathbb R$ is still not restricted to be positive as required in the linear program on standard form (1). Hence again decomposition into positive and negative part is used

$$\theta = \theta^+ - \theta^- $$

where again $\theta^+=max(0,\theta)$ is positive part and $\theta^- = \max(0,-\theta)$ is negative part. The $N$ constraints can then be written as

$$\mathbf y:= \begin{bmatrix} y_1 \\ \vdots \\ y_N\end{bmatrix} = \begin{bmatrix} \mathbf x_1^\top \\ \vdots \\ \mathbf x_N^\top \end{bmatrix}(\theta^+ - \theta^-) + \mathbf I_Nu - \mathbf I_Nv ,$$

where $\mathbf I_N = diag\{\mathbf 1_N\}$.

Next define $b:=\mathbf y$ and the design matrix $\mathbf X$ storing data on independent variables as

$$ \mathbf X := \begin{bmatrix} \mathbf x_1^\top \\ \vdots \\ \mathbf x_N^\top \end{bmatrix} $$

To rewrite constraint:

$$b= \mathbf X(\theta^+ - \theta^-) + \mathbf I_N u- \mathbf I_N v= [\mathbf X , -\mathbf X , \mathbf I_N ,\mathbf - \mathbf I_N] \begin{bmatrix} \theta^+ \\ \theta^- \\ u \\ v\end{bmatrix}$$

Define the $(N \times 2K + 2N )$ matrix

$$A := [\mathbf X , -\mathbf X , \mathbf I_N ,\mathbf - \mathbf I_N]$$

and introduce $\theta^+$ and $\theta^-$ as variables over which to minimize so they are part of $z$ to get

$$b = A \begin{bmatrix} \theta^+ \\ \theta^- \\ u \\ v\end{bmatrix} = Az$$

Because $\theta^+$ and $\theta^-$ only affect the minimization problem through the constraint a $\mathbf 0$ of dimension $2K\times 1$ must be introduced as part of the coeffient vector $c$ which can the appropriately be defined as

$$ c = \begin{bmatrix}\mathbf 0 \\ \tau \mathbf 1_N \\ (1-\tau) \mathbf 1_N \end{bmatrix},$$

thus ensuring that $c^\top z = \underbrace{\mathbf 0^\top(\theta^+ - \theta^-)}_{=0}+\tau \mathbf 1_N^\top u + (1-\tau)\mathbf 1_N^\top v = \sum_{i=1}^N \rho_\tau(\epsilon_i).$

Hence $c,A$ and $b$ are then defined and the program as given in $(1)$ completely specified.

This is probably best digested using an example. To solve this in R use the package quantreg by Roger Koenker. Here is also illustration of how to set up the linear program and solve with a solver for linear programs:

base=read.table("http://freakonometrics.free.fr/rent98_00.txt",header=TRUE)

attach(base)

library(quantreg)

library(lpSolve)

tau <- 0.3

# Problem (1) only one covariate

X <- cbind(1,base$area)

K <- ncol(X)

N <- nrow(X)

A <- cbind(X,-X,diag(N),-diag(N))

c <- c(rep(0,2*ncol(X)),tau*rep(1,N),(1-tau)*rep(1,N))

b <- base$rent_euro

const_type <- rep("=",N)

linprog <- lp("min",c,A,const_type,b)

beta <- linprog$sol[1:K] - linprog$sol[(1:K+K)]

beta

rq(rent_euro~area, tau=tau, data=base)

# Problem (2) with 2 covariates

X <- cbind(1,base$area,base$yearc)

K <- ncol(X)

N <- nrow(X)

A <- cbind(X,-X,diag(N),-diag(N))

c <- c(rep(0,2*ncol(X)),tau*rep(1,N),(1-tau)*rep(1,N))

b <- base$rent_euro

const_type <- rep("=",N)

linprog <- lp("min",c,A,const_type,b)

beta <- linprog$sol[1:K] - linprog$sol[(1:K+K)]

beta

rq(rent_euro~ area + yearc, tau=tau, data=base)