So, I have been wondering about an interesting observation. My data contains 1006 log-returns of the SP500-index and I've estimated a GARCH(1,1)-process with Gaussian quasi-maximum likelihood - eventhough the logreturns is fitted best by a Student's t-distribution.

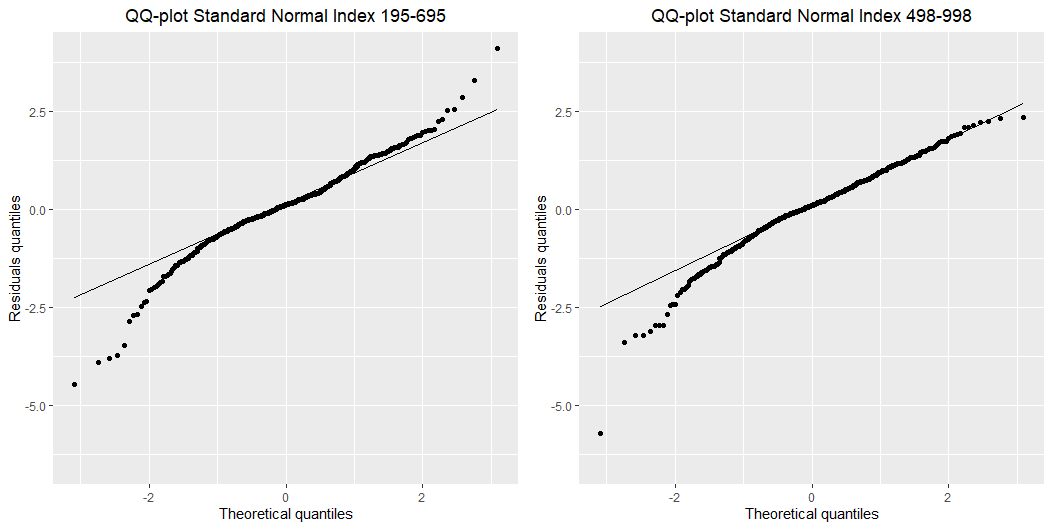

I was interested in some goodness of fit arguments and was wondering about different periods of my data and how the GARCH(1,1)-process fits the different periods. I found out the best AIC-value was produced by the indices 195-695 (500 observations fitted) $$\text{AIC}_{\text{best}}=-7.556248$$ and the worst produced by the indicies (498-998) $$\text{AIC}_{\text{worst}}=-6.763304.$$ But when I look at the densities of the standardized residuals from those two periods and QQ-plots against a standard normal distribution my result is quite disturbing and I cannot find the intuition behind it.

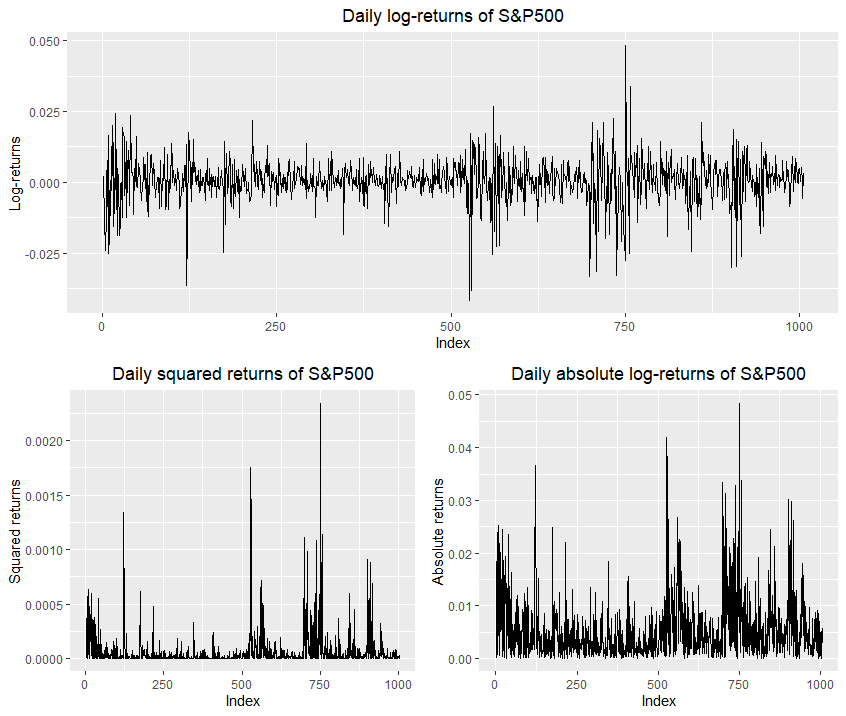

This is the log-returns plot I'm looking at:

And these are the QQ-plots:

I was thinking that it might had something to do with the stationarity. It's clear that in the period of indicies 195-695 I have "more" stationarity in the period of indicies 468-998. But since I use Gaussian quasi-maximum likelihood (assuming the noise process is standard Gaussian), how do one explain the "bad" fit on the "good" standardized residuals? Thank you in advance.

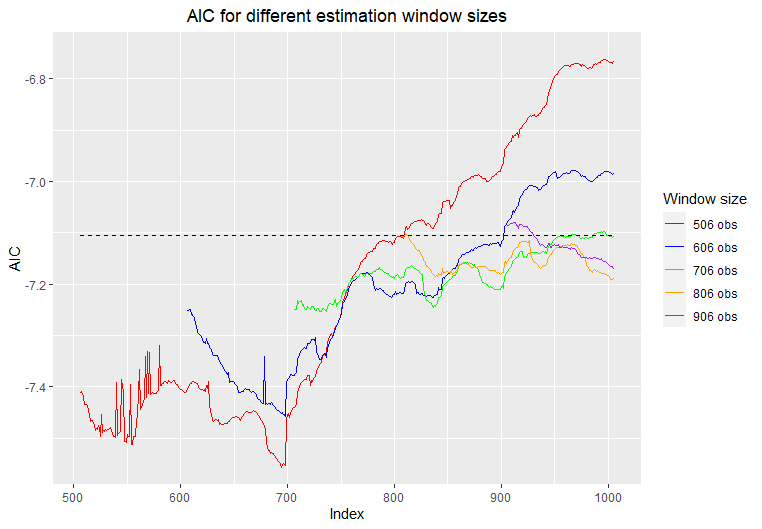

AIC plot