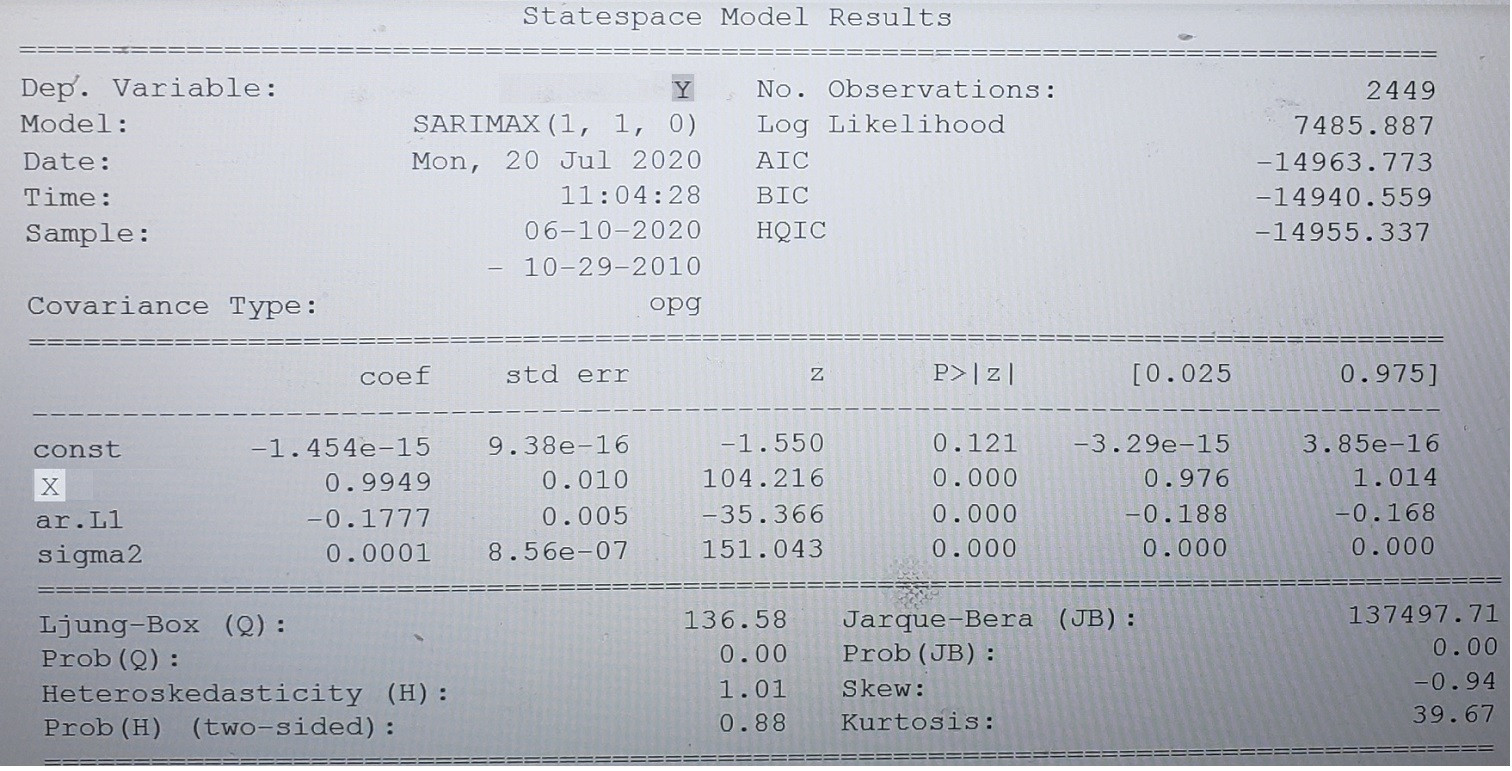

I have fit an ARIMAX (1, 1, 0) model to a timeseries dataset consisting of 1 endogenous timeseries ("Y") and 1 exogenous timeseries ("X"). My exogenous timeseries in the model was defined as sm.add_constant(df["X"]). Stationarity and invertibility were enforced in the Statsmodels SARIMAX model.

The output of the model is as seen in the attached image:

For the fourth to the last record in the timeseries:

- the model's predicted (and fitted) value is 6.58713620525664

- the Y value is 6.5895

- the X value is 6.6768

For the third to the last record in the timeseries:

- the model's predicted (and fitted) value is 6.59034839014186

- the Y value is 6.609

- the X value is 6.67855

For the record before the last record in the timeseries:

- the model's predicted (and fitted) value is 6.61892751060232

- the Y value is 6.5815

- the X value is 6.6917

For the last (oldest) record in the timeseries:

- the model's predicted (and last fitted) value is 6.56786815053348

- the Y value is 6.5805

- the X value is 6.67075

For the first prediction:

- the model's predicted value is 6.59319101863394

- the X value is 6.68705

- (There is no Y value)

I have tried to recreate the predicted values manually without any success. Can anyone help, please?