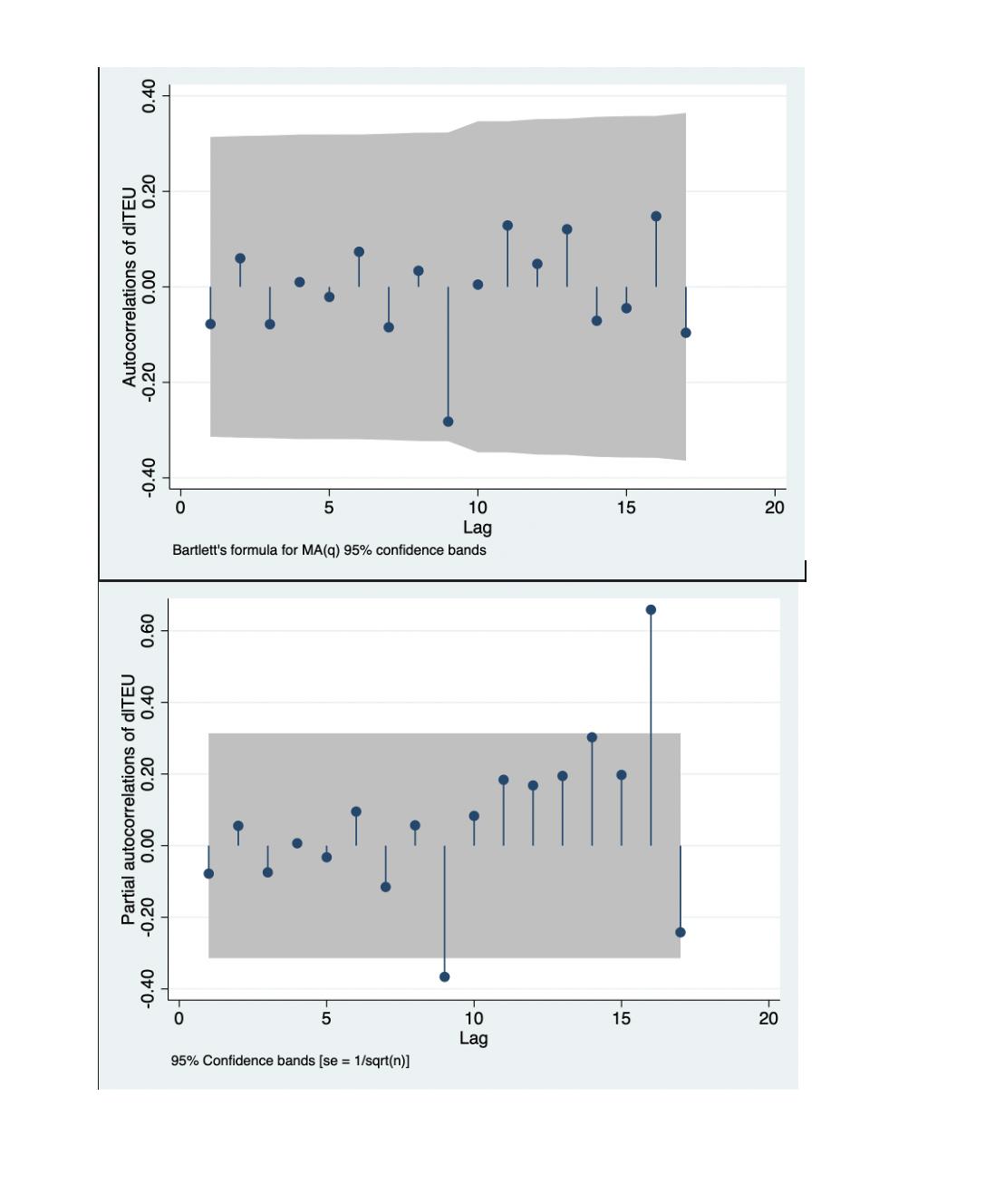

Since you provided ACF and PACF plots only for differentiated time series, so I can't tell you anything about the original one.

As you can clearly see on the plots, there's no significant autocorrelations in your time series (i.e. values for first lags are not significant). So, you have to choose $p=q=0$ in ARIMA model.

But there's something that points to possible seasonality existence - significant PACF for lags 9 and 16. However, this is only a hypothesis and it needs to be checked more precisely by using, for instance, spectral analysis. But first you need to explore ACF and PACF for more lags.

One more thing to check. What implies a non-stationarity in an original series? Maybe it was a deterministic trend that should be removed just by subtracting it instead of differentiating. Subtracting deterministic trend preserves more information in the processed time series.