To clarify, by a Simple Random Walk I mean

$$ Y_i = \begin{cases} -1 & prob = 1/2\\ 1 & prob = 1/2 \end{cases} $$ $$ X_t = \sum_{i=1}^t{Y_i} \quad \textrm{,}\,X_0 = 0 $$

and by Random Walk I mean

$$ X_t = X_{t-1} + \epsilon \quad ,\,X_0 = 0 \quad and \quad \epsilon \sim N(0, 1) $$

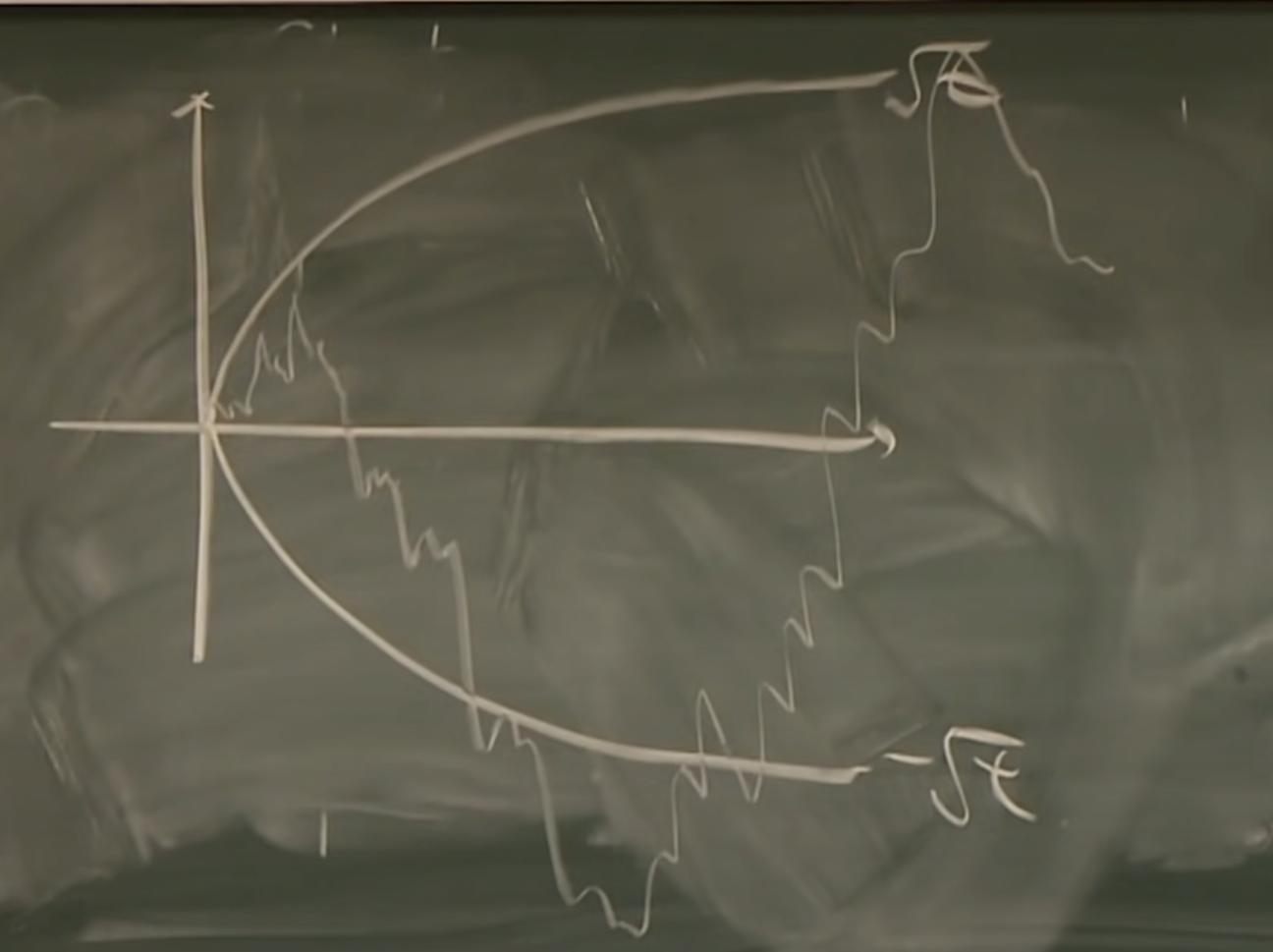

While I see how they differ, it is also my intuition that they follow similar patterns. Simple Random Walk is stationary, because in any interval what happens is irrelevant of the starting point and the distribution is the same as in any other interval. Also the values will not explode to $Y=X$ or $Y=-X$, because in the long run they will be contained in a cone shaped region (on the image below) with values $\sim N(0, \sqrt{t})$. This also means that the values will somewhat oscillate around $0$, which is quite stationary.

What is different about Random Walk, that it does not have the same properties and is not stationary?

in any interval what happens is irrelevant of the starting point and the distribution is the same as in any other intervalare not my ideas, but I have taken them from an MIT lecture. I have heard that there are a few definitions of stationarity, am I maybe confusing some of them, or is something else going on here? $\endgroup$