I have a fundamental question regarding the applications of the results of PCA:

If we have already performed a successful PCA on a dataset of, say, real estate prices of a certain region over the last 20 years, then we've figured out the Eigenvalues and Eigenvectors that maximize the explanatory power of a mathematically descriptive system, while simultaneously lowering its complexity.

If we're now 2 years into the future and possess new real estate prices, how can we judge if certain real estate is under- or overvalued with these PCA results from the initial dataset?

Do we have to apply a new PCA on a dataset that contains the initial 20 years as well as the 2 future years of data in order to make such an assessment?

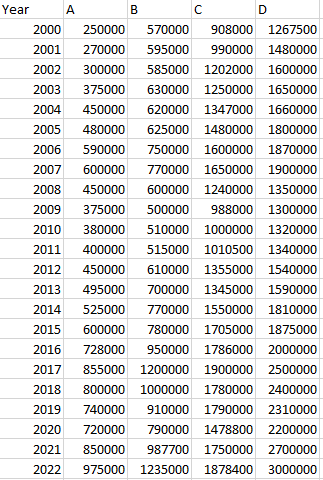

This is the initial dataset:

Here are the eigenvectors and values:

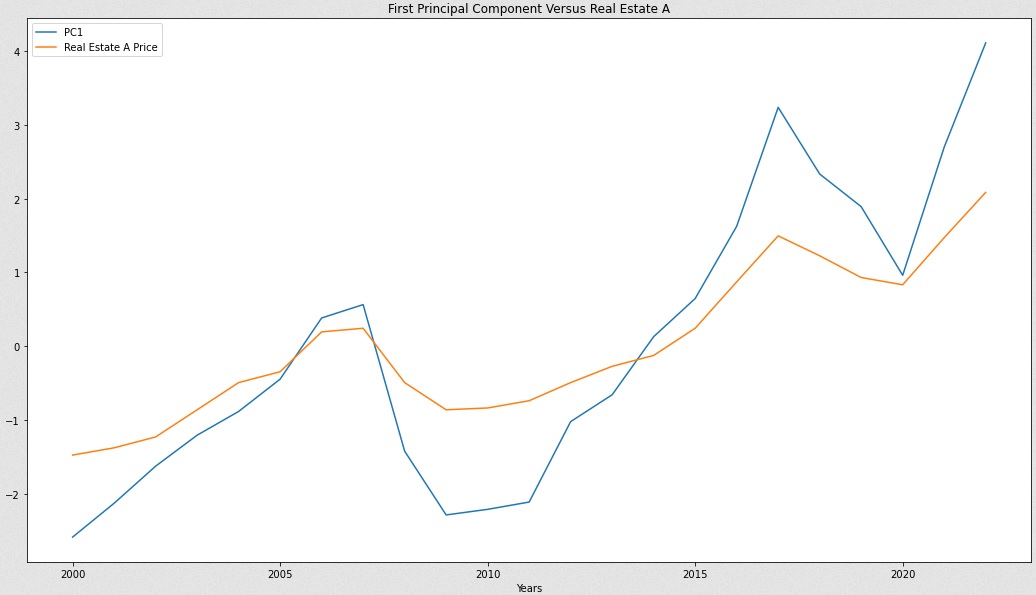

Here's the result that I get when I înclude all 22 years of data, plot the first column of the PC matrix and compare it against the standardized price of a real estate A:

I've generated eigenvector and eigenvalue tables with the scikit tools and then I calculated the dot product between the standardized price matrix and the eigenvector matrix to get a principal components matrix. The blue line reprsents the first column of this PC matrix and the orange line is the standardized Real Estate A price.

Is this how it's supposed to be used? You always need to include the latest data so as to see the most accurate discrepancies between modeled PCA value and the real current real estate value?

time-seriestag to your question, to get the attention of those more knowledgeable than I in applications to time series. In your example, essentially all of the variance in the predictors is captured in the first principal component, meaning that all 4 predictors are highly correlated among each other. Spurious correlation would seem to be a big danger. $\endgroup$