I personally prefer working with R, which has much better facilities for time series forecasting. First off, your series has such high counts that count models are probably not going to give you much better results than straightforward time series methods. Yes, these typically assume normally distributed innovations, and your prediction intervals will go below zero, but they are much better tested and understood than count data models.

Let's first plot your data.

tickets <- ts(c(15, 26, 21, 23, 31, 61, 27, 35, 2, 27, 37, 30, 26,

13, 19, 11, 27, 30, 55, 103, 23, 59, 72, 57, 23, 53, 60, 46,

100, 31, 15, 8, 20, 92, 49, 29, 60, 16, 10, 63, 12, 71, 114, 66,

27, 4, 20, 85, 67, 24, 62, 18, 5, 22, 43, 28, 27, 106, 87, 3, 53,

22, 11, 27, 76, 55, 67, 35, 50, 68, 133, 55, 78, 14, 76, 111, 132,

174, 168), frequency=7)

library(forecast)

training <- ts(tickets[1:41], frequency=7)

test <- ts(tickets[42:length(tickets)],start=c(6,7), frequency=7)

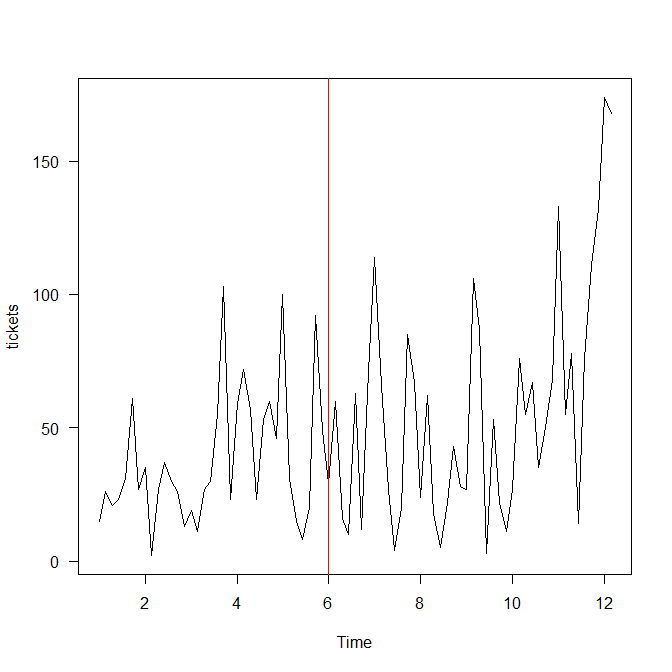

plot(tickets, las=1)

abline(v=end(training), col="red")

"Time" on the horizontal axis refers to weeks. The red line shows the end of your training data. We already see the first problem: the variance is increasing. Compare the first three weeks to everything after, and then the last two data points. These will be very hard to forecast, because (a) we have never seen anything like this, and (b) there is no obvious trend we would be justified in extrapolating.

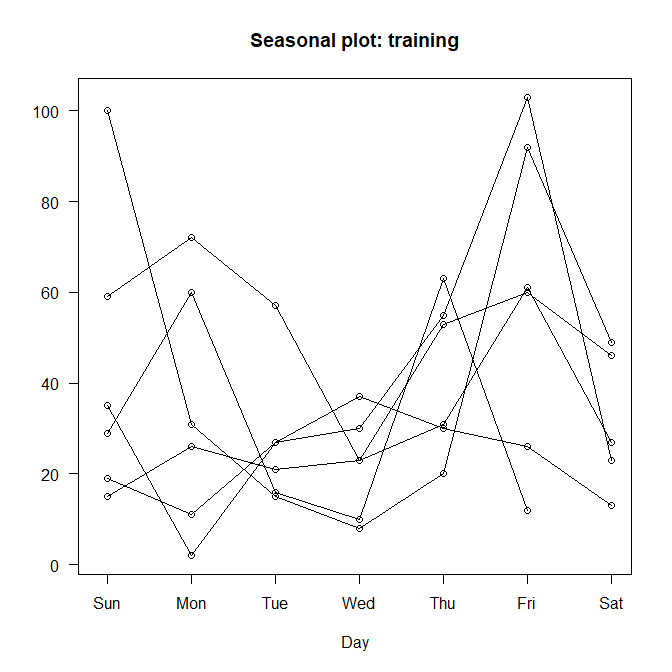

Here is a seasonplot of your training data:

seasonplot(training)

The day-of-week seasonality is not really obvious. The slump on Wednesday is really more driven by fewer large observations there than on other days, but especially with only six weeks of training data, it could just be coincidence that none of the high values happened to fall on a Wednesday. A forecasting algorithm may or may not believe this series is seasonal.

Let's fit an ARIMA model:

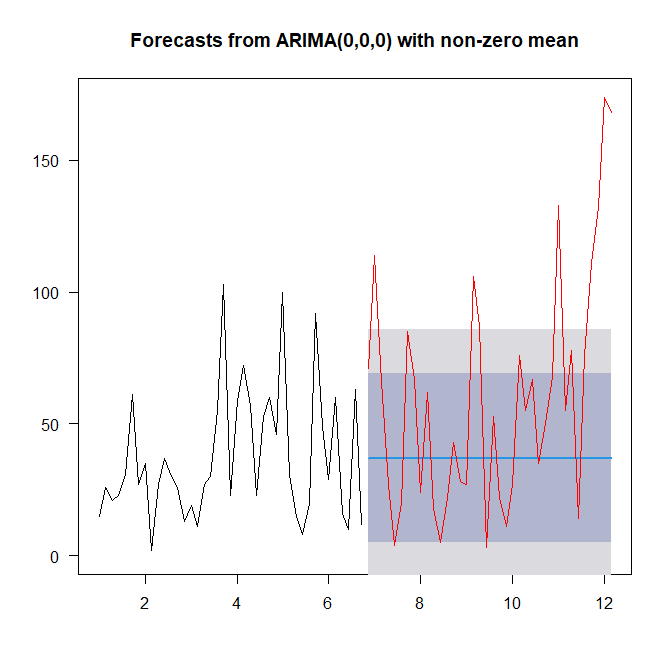

model_arima <- auto.arima(training)

summary(model_arima)

plot(forecast(model_arima,h=length(test)),ylim=c(0,max(tickets)), las=1)

lines(test,col="red")

forecast::auto.arima() fits a simple mean model and extrapolates this out. This is often a very good idea. We see too many values fall outside the prediction interval, because of the increasing variance.

Let's also try an exponential smoothing model:

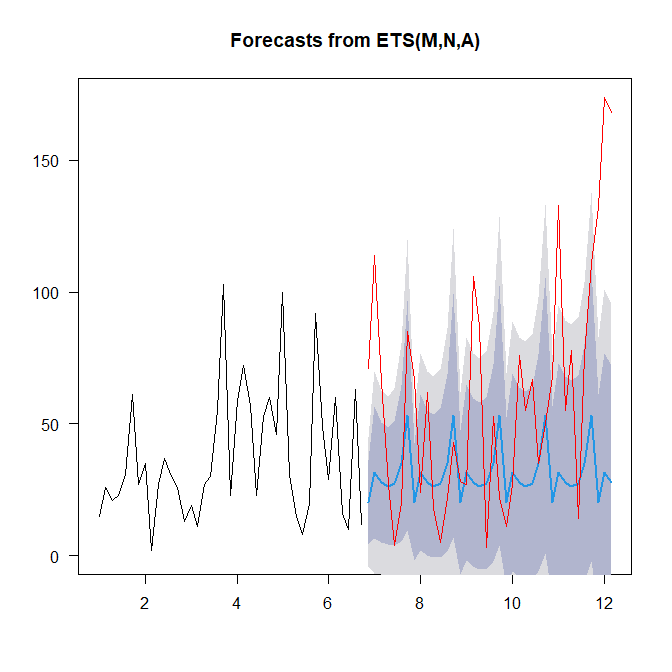

model_ets <- ets(training)

summary(model_ets)

plot(forecast(model_ets,h=length(test)),ylim=c(0,max(tickets)), las=1)

lines(test,col="red")

Here, forecast::ets() sees a multiplicative error (that's the M), no trend (the N) and additive seasonality (the A). The forecast looks much more sophisticated - but that is no guarantee of better performance (see the link above), and we see about as many actuals outside the prediction intervals.

In terms of test set accuracy, the ARIMA model (that is, the flat mean forecast) outperforms the ETS model on RMSE (which is the only error measure I would trust here):

> accuracy(forecast(model_arima,h=length(test)),test)

ME RMSE MAE MPE MAPE MASE ACF1 Theil's U

Training set -8.661690e-12 24.63984 20.09756 -88.22527 116.1325 0.7617805 0.1347019 NA

Test set 2.310526e+01 49.33345 37.21053 -62.02226 123.7165 1.4104324 0.4915275 0.5122738

> accuracy(forecast(model_ets,h=length(test)),test)

ME RMSE MAE MPE MAPE MASE ACF1 Theil's U

Training set 0.6067627 22.57793 17.95465 -69.08313 101.1897 0.6805555 0.07025731 NA

Test set 28.8387549 53.09292 38.89982 -28.61668 100.4135 1.4744635 0.50643194 0.5132892

I hasten to add that the forecast and the newer fable packages from the same author are the gold standard in automatic time series forecasting.

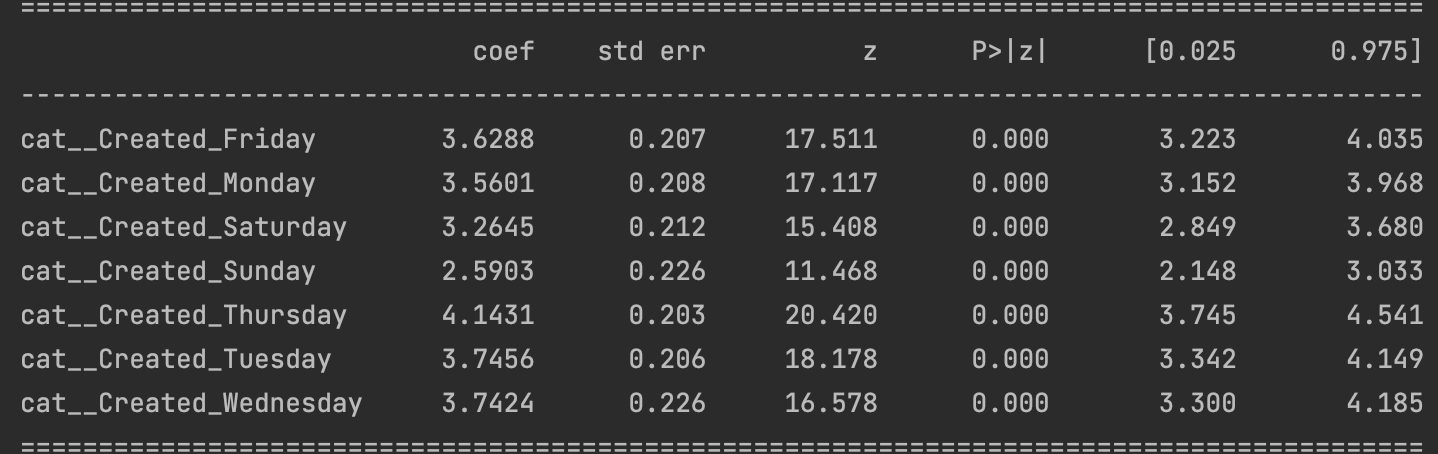

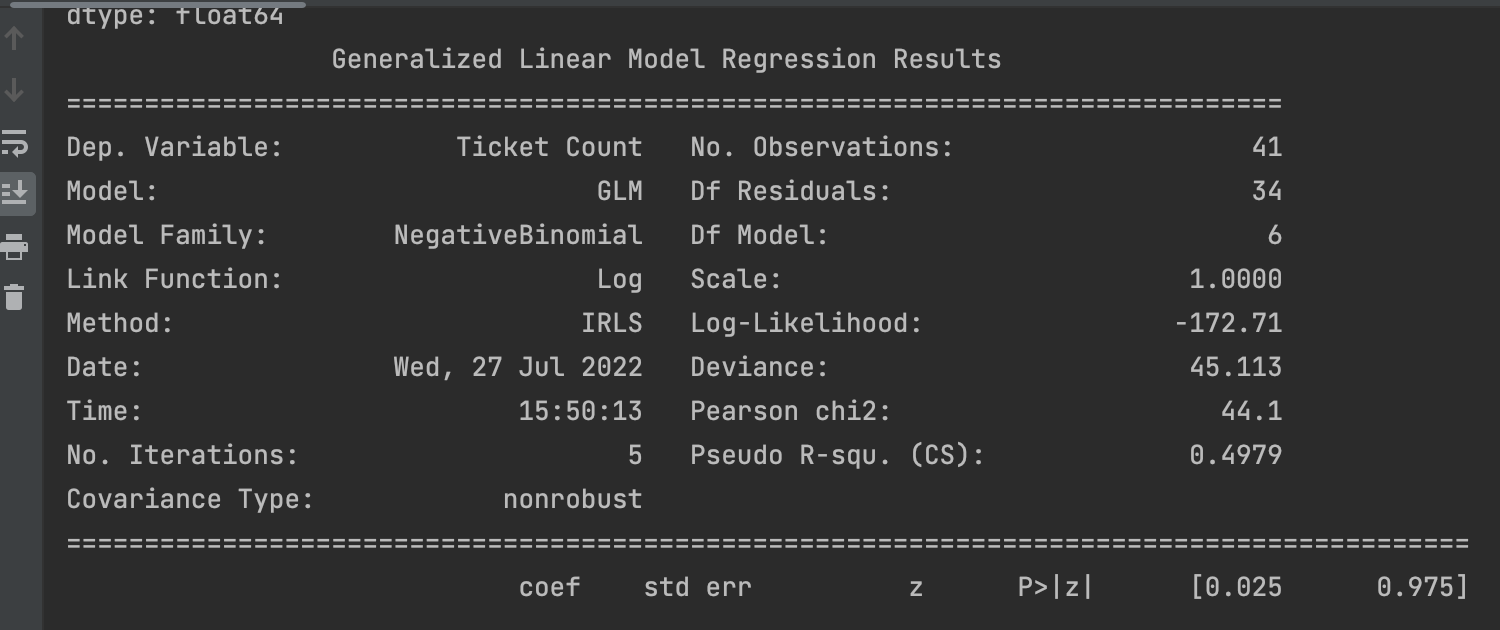

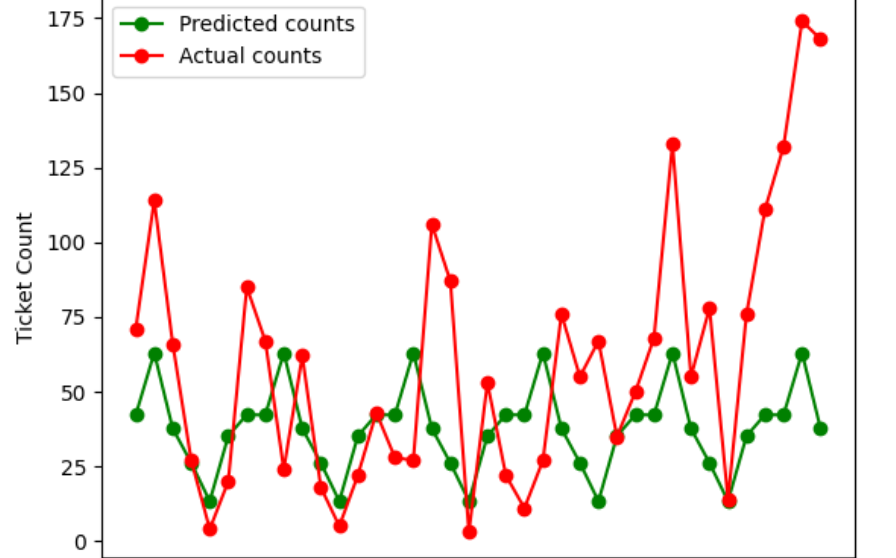

I don't think running a negbin or any other regression will give you better results. You have very little data, and fitting seven parameters with only 41 data points is a lot to expect.

The key problem is the increasing variance, and especially the very high two last values. Your best bet might be to try to figure out whether anything special happened there that you could model. If these were movie theater ticket sales, then it would be good to learn which movies opened in which week, and whether COVID restrictions were in place, or some such. This may be useful.

The forecasting tag wiki contains pointers to excellent resources on forecasting.