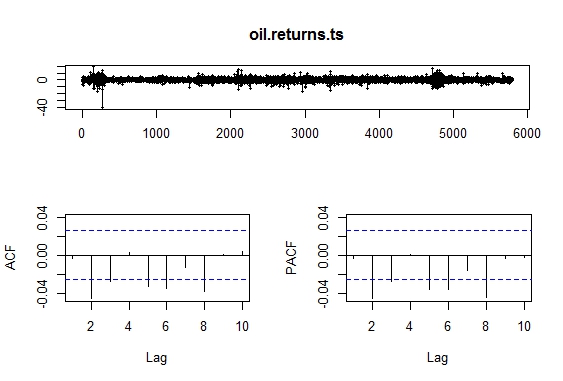

So I plotted the ACF/PACF of oil returns and was expecting to see some positive autocorrelation but to my surprise I only get negative significant autocorrelation. How should I interpret the above graph? They seem to indicate that there is a tendency for oil returns to increase when it decreased previously and vice-versa, thus the oscillating behaviour. Please correct me if I'm wrong.