We can find different Resampling methods: or loosely called "simulation" methods that depend upon resampling or suffling of the samples. There might be difference in opinion on what is called what and what is proper names etc. The following discussion tries to generalized and simplify what is available in text.

Resampling methods are used in (1) estimating precision / accuracy of sample statistics through using subset of data (e.g. Jackknifing) or drawing randomly with replacement from a set of data points (e.g. bootstrapping) (2) Exchanging labels on data points when performing significance tests (permutation tests, also called exact tests, randomization tests, or re-randomization tests) (3) Validating models by using random subsets (bootstrapping, cross validation) (see wikipedia: resampling methods)

"Bootstrapping is a statistical method for estimating the sampling distribution of an estimator by sampling with replacement from the original sample". The method assigns measures of accuracy (defined in terms of bias, variance, confidence intervals, prediction error or some other such measure) to sample estimates.

The basic idea of bootstrapping is that inference about a population from sample data (sample → population) can be modeled by resampling the sample data and performing inference on (resample → sample). As the population is unknown, the true error in a sample statistic against its population value is unknowable. In bootstrap-resamples, the 'population' is in fact the sample, and this is known; hence the quality of inference from resample data → 'true' sample is measurable." see wikipedia

Yvar <- c(8,9,10,13,12, 14,18,12,8,9, 1,3,2,3,4)

#To generate a single bootstrap sample

sample(Yvar, replace = TRUE)

#generate 1000 bootstrap samples

boot <-list()

for (i in 1:1000)

boot[[i]] <- sample(Yvar,replace=TRUE)

In univariate problems, it is usually acceptable to resample the individual observations with replacement ("case resampling"). Here we resample the data with replacement, and the size of the resample must be equal to the size of the original data set.

In regression problems, case resampling refers to the simple scheme of resampling individual cases - often rows of a data set in regression problems, the explanatory variables are often fixed, or at least observed with more control than the response variable. Also, the range of the explanatory variables defines the information available from them. Therefore, to resample cases means that each bootstrap sample will lose some information (see Wikipedia). So it will be logical to sample rows of the data rather just Yvar.

Yvar <- c(8,9,10,13,12, 14,18,12,8,9, 1,3,2,3,4)

Xvar <- c(rep("A", 5), rep("B", 5), rep("C", 5))

mydf <- data.frame (Yvar, Xvar)

boot.samples <- list()

for(i in 1:10) {

b.samples.cases <- sample(length(Xvar), length(Xvar), replace=TRUE)

b.mydf <- mydf[b.samples.cases,]

boot.samples[[i]] <- b.mydf

}

str(boot.samples)

boot.samples[1]

You can see some cases are repeated as we are sampling with replacement.

"Parametric bootstrap - a parametric model is fitted to the data, often by maximum likelihood, and samples of random numbers are drawn from this fitted model. Usually the sample drawn has the same sample size as the original data. Then the quantity, or estimate, of interest is calculated from these data. This sampling process is repeated many times as for other bootstrap methods. The use of a parametric model at the sampling stage of the bootstrap methodology leads to procedures which are different from those obtained by applying basic statistical theory to inference for the same model."(see Wikipedia). The following is parametric bootstrap with normal distribution assumption with mean and standard deviation parameters.

Yvar <- c(8,9,10,13,12, 14,18,12,8,9, 1,3,2,3,4)

# parameters for Yvar

mean.y <- mean(Yvar)

sd.y <- sd(Yvar)

#To generate a single bootstrap sample with assumed normal distribution (mean, sd)

rnorm(length(Yvar), mean.y, sd.y)

#generate 1000 bootstrap samples

boot <-list()

for (i in 1:1000)

boot[[i]] <- rnorm(length(Yvar), mean.y, sd.y)

There are other variants of bootstrap, please consult the wikipedia page or any good statical book on resampling.

"The jackknife estimator of a parameter is found by systematically leaving out each observation from a dataset and calculating the estimate and then finding the average of these calculations. Given a sample of size N, the jackknife estimate is found by aggregating the estimates of each N − 1 estimate in the sample." see: wikipedia The following shows how to jackknife the Yvar.

jackdf <- list()

jack <- numeric(length(Yvar)-1)

for (i in 1:length (Yvar)){

for (j in 1:length(Yvar)){

if(j < i){

jack[j] <- Yvar[j]

} else if(j > i) {

jack[j-1] <- Yvar[j]

}

}

jackdf[[i]] <- jack

}

jackdf

"the regular bootstrap and the jackknife, estimate the variability of a statistic from the variability of that statistic between subsamples, rather than from parametric assumptions. For the more general jackknife, the delete-m observations jackknife, the bootstrap can be seen as a random approximation of it. Both yield similar numerical results, which is why each can be seen as approximation to the other." See this question on Bootstrap vs Jacknife.

According to wikipedia "A permutation test (also called a randomization test, re-randomization test, or an exact test) is a type of statistical significance test in which the distribution of the test statistic under the null hypothesis is obtained by calculating all possible values of the test statistic under rearrangements of the labels on the observed data points. Permutation tests exist for any test statistic, regardless of whether or not its distribution is known. Thus one is always free to choose the statistic which best discriminates between hypothesis and alternative and which minimizes losses."

The difference between permutation and bootstrap is that bootstraps sample with replacement, and permutations sample without replacement. In either case, the time order of the observations is lost and hence volatility clustering is lost — thus assuring that the samples are under the null hypothesis of no volatility clustering.

The permutations always have all of the same observations, so they are more like the original data than bootstrap samples. The expectation is that the permutation test should be more sensitive than a bootstrap test. The permutations destroy volatility clustering but do not add any other variability.

See the question on permutation vs bootstrapping - "The permutation test is best for testing hypotheses and bootstrapping is best for estimating confidence intervals".

So to perform permutation in this case we can just change replace = FALSE in the above bootstrap example.

Yvar <- c(8,9,10,13,12, 14,18,12,8,9, 1,3,2,3,4)

#generate 1000 bootstrap samples

permutes <-list()

for (i in 1:1000)

permutes[[i]] <- sample(Yvar,replace=FALSE)

In case of more than one variable, just picking of the rows and reshuffling the order will not make any difference as the data will remain same. So we reshuffle the y variable. Something what you have done, but I do not think we do not need double reshuffling of both x and y variables (as you have done).

Yvar <- c(8,9,10,13,12, 14,18,12,8,9, 1,3,2,3,4)

Xvar <- c(rep("A", 5), rep("B", 5), rep("C", 5))

mydf <- data.frame (Yvar, Xvar)

permt.samples <- list()

for(i in 1:10) {

t.yvar <- Yvar[ sample(length(Yvar), length(Yvar), replace=FALSE) ]

b.df <- data.frame (Xvar, t.yvar)

permt.samples[[i]] <- b.df

}

str(permt.samples)

permt.samples[1]

"Monte Carlo methods (or Monte Carlo experiments) are a broad class of computational algorithms that rely on repeated random sampling to obtain numerical results; typically one runs simulations many times over in order to obtain the distribution of an unknown probabilistic entity. The name comes from the resemblance of the technique to the act of playing and recording results in a real gambling casino. " see Wikipedia

"In applied statistics, Monte Carlo methods are generally used for two purposes:

(1) To compare competing statistics for small samples under realistic data conditions. Although Type I error and power properties of statistics can be calculated for data drawn from classical theoretical distributions (e.g., normal curve, Cauchy distribution) for asymptotic conditions (i. e, infinite sample size and infinitesimally small treatment effect), real data often do not have such distributions.

(2) To provide implementations of hypothesis tests that are more efficient than exact tests such as permutation tests (which are often impossible to compute) while being more accurate than critical values for asymptotic distributions.

Monte Carlo methods are also a compromise between approximate randomization and permutation tests. An approximate randomization test is based on a specified subset of all permutations (which entails potentially enormous housekeeping of which permutations have been considered). The Monte Carlo approach is based on a specified number of randomly drawn permutations (exchanging a minor loss in precision if a permutation is drawn twice – or more frequently—for the efficiency of not having to track which permutations have already been selected)."

Both MC and Permutation test are sometime collectively called randomization tests. The difference is in MC we sample the permutation samples, rather using all possible combinations [see] 18.

The idea beyond cross validation is that models should be tested with data that were not used to fit the model. Cross validation is perhaps most often used in the context of prediction.

"Cross-validation is a statistical method for validating a predictive model. Subsets of the data are held out for use as validating sets; a model is fit to the remaining data (a training set) and used to predict for the validation set. Averaging the quality of the predictions across the validation sets yields an overall measure of prediction accuracy.

One form of cross-validation leaves out a single observation at a time; this is similar to the jackknife. Another, K-fold cross-validation, splits the data into K subsets; each is held out in turn as the validation set." see Wikipedia . Cross validation is usually done with quantitative data. You can convert your qualitative (factor data) to quantitative someway to fit a linear model and test this model. The following is simple hold-out strategy where 50% of data is used for model prediction while rest is used for testing. Lets assume Xvar is also quantitative variable.

Yvar <- c(8,9,10,13,12, 14,18,12,8,9, 1,3,2,3,4)

Xvar <- c(rep(1, 5), rep(2, 5), rep(3, 5))

mydf <- data.frame (Yvar, Xvar)

training.id <- sample(1:nrow(mydf), round(nrow(mydf)/2,0), replace = FALSE)

test.id <- setdiff(1:nrow(mydf), training.id)

# training dataset

mydf.train <- mydf[training.id]

#testing dataset

mydf.test <- mydf[test.id]

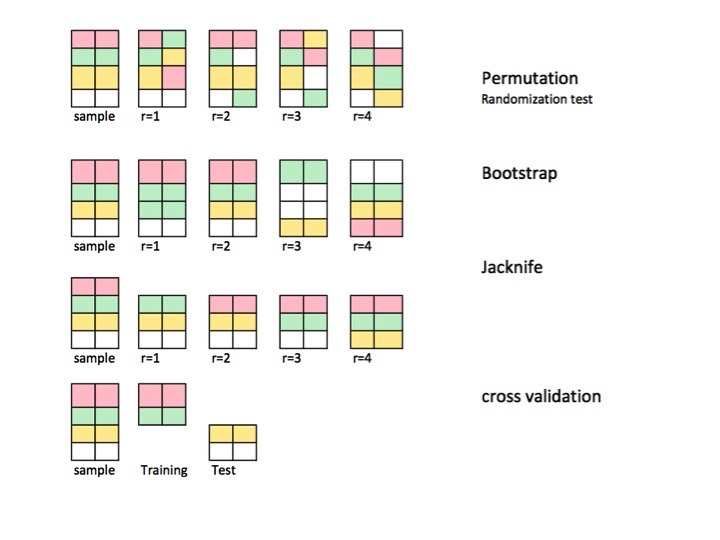

Unlike bootstrap and permutation tests the cross-validation dataset for training and testing is different. The following figure shows a summary of resampling in different methods.

Hope this helps a bit.