You construct the policy dummy the way you first describe it, i.e. create a column of zeroes. Then for each firm you replace this with ones if a firm is in the treatment group AND it is in the post-treatment period. Something like this

$$ \begin{array}{ccccc} \text{firm} & \text{time} & \text{treated} & \text{post} & \text{policy} \\ \hline 1 & 1 & 0 & 0 & 0 \\ 1 & 2 & 0 & 0 & 0 \\ 1 & 3 & 0 & 1 & 0 \\ 1 & 4 & 0 & 1 & 0 \\ \hline 2 & 1 & 1 & 0 & 0 \\ 2 & 2 & 1 & 0 & 0 \\ 2 & 3 & 1 & 1 & 1 \\ 2 & 4 & 1 & 1 & 1 \\ \hline 3 & 1 & 1 & 0 & 0 \\ 3 & 2 & 1 & 0 & 0 \\ 3 & 3 & 1 & 0 & 0 \\ 3 & 4 & 1 & 1 & 1 \\ \end{array} $$

where $\text{post}$ is an indicator for the post treatment period. In your equation above, the $\alpha_0$ and $\text{Treat}_i$ are going to be absorbed in the firm fixed effects.

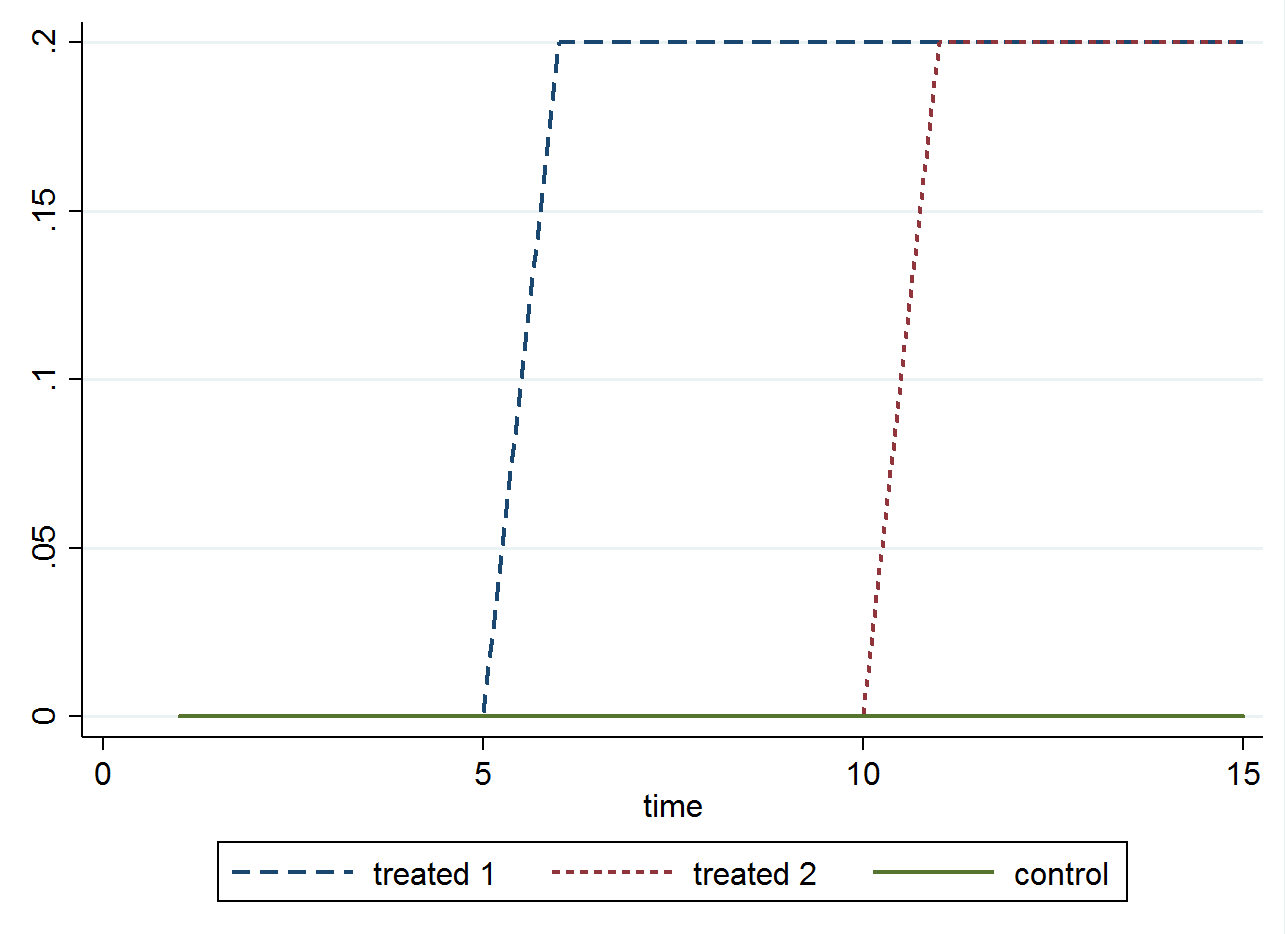

Regarding the interpretation, this setting makes an assumption which I probably did not state in the previous answer. The assumption is that the treatment effect is the same across all periods. This means that if a firm is treated yesterday and has a gain of 2, then a firm which is treated today also has a gain of 2 (relative to firms which are never treated). I made a graph to show what this assumption means

In case you would like a reference for this, you can check out Jeff Wooldridge's notes on difference in differences and the section on extensions for multiple groups and time periods: http://www.nber.org/WNE/Slides7-31-07/slides_10_diffindiffs.pdf (What’s New in Econometrics? Lecture 10 Difference-in-Differences Estimation, Wooldridge 2007).