I have a time series and I'd like to do a simulation of log-returns using the normalization with Johnson distribution.

library(JohnsonDistribution)

library(moments)

rm(list=ls(all=TRUE))

set.seed(1)

n <- 252

log_mydata1 <- runif(n, min=-0.06, max= 0.05)

m1 <- mean(log_mydata1)

var1 <- sd(log_mydata1)

sk1 <- skewness(log_mydata1)

k1 <- kurtosis(log_mydata1)

# Fitting Johnson distribution parameters and type

FitJohnsonDistribution(m1, var1, sk1, k1)

iType <- FitJohnsonDistribution(m1, var1, sk1, k1)[1]

gamma <- FitJohnsonDistribution(m1, var1, sk1, k1)[2]

delta <- FitJohnsonDistribution(m1, var1, sk1, k1)[3]

lambda <- FitJohnsonDistribution(m1, var1, sk1, k1)[4]

xi <- FitJohnsonDistribution(m1, var1, sk1, k1)[5]

# Applying Johnson transformation

z1 <- zJohnsonDistribution(log_mydata1, iType, gamma, delta, lambda , xi)

shapiro.test(z1) # W = 0.99374, p-value = 0.377

I have used the code and fitted my random data and log-returns were fitted with ARIMA(3,0,2) model. Then I applied some test to check the model quality.

# Fitting ARMA model

ArimaModelFit <- function(z)

{

final.aic <- Inf

final.order <- c(0,0,0)

for (p in 0:3)

for (q in 0:3)

{

if ( p == 0 && q == 0) {

next

}

arimaFit = tryCatch( arima(z, order=c(p, 0, q)),

error=function( err ) FALSE,

warning=function( err ) FALSE )

if( !is.logical( arimaFit ) ) {

current.aic <- AIC(arimaFit)

if (current.aic < final.aic) {

final.aic <- current.aic

final.order <- c(p, 0, q)

final.arima <- arima(z, order=final.order)

}

} else {

next

}

}

result <- list(aic=final.aic, order=final.order, arima=final.arima)

return(result)

} # function

f1 <- ArimaModelFit(z1)

rf1 <- residuals(f1$arima); shapiro.test(rf1) # W = 0.9944, p-value = 0.4785

Then I simulated data with the ARIMA model

#ARMA Simulation

sim <- arima.sim(list(order = c(3,0,2),

ar = c(f1$arima$coef[1], f1$arima$coef[2], f1$arima$coef[3]),

ma = c(f1$arima$coef[4], f1$arima$coef[5])), n = n)

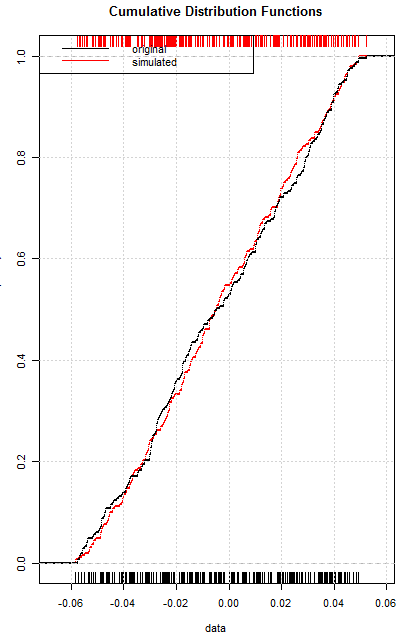

Finally, I'd like to inverse the fitted data and to chect the quality of simulation with Kolmogorov-Smirnov test and Cumulative Distribution Functions (CDFs) of marginal (log-returns) and simulated (y) data.

# Applying inverse of Johnson transformation

y <- yJohnsonDistribution(sim, iType, gamma, delta, lambda , xi)

# Two-sample Kolmogorov-Smirnov test

ks.test(log_mydata1, y) #D = 0.048552, p-value = 0.9283

Fn = ecdf(log_mydata1)

Fm = ecdf(y)

plot(Fn,

main="Cumulative Distribution Functions",

xlab="data",

ylab="Cumulative Frequency",

pch=NA, lwd= 2,

col = "red")

lines(Fm, pch=NA, lty=1, lwd= 2)

rug(log_mydata1)

rug(y, side = 3, col = "red")

legend("topleft",

legend=c("original", "simulated"),

lty=c(1,1),

col=c("black", "red"))

grid()

The p-value of Kolmogorov-Smirnov test is 0.9283 and CDFs are close each to other.

But according to the documentaion of the JohnsonDistribution package I should use the zJohnsonDistribution function instead of the yJohnsonDistribution function.

Also I confused with sim series. In my case, sim is the normal distributed variable, but it is should be uniformly distributed on the unit interval [0, 1].

Questions. Am I correct in my steps? How to inverse correctly the Johnson normalized variable to a marginal variable? Should I use the qnorm() function?