When the predicted future value actually materializes, does it matter if it is outside the predicted confidence interval?

The value of prediction intervals is that they express the uncertainty in the forecasts. If we only produce point forecasts, there is no way of telling how accurate the forecasts are. However, if we also produce prediction intervals, then it is clear how much uncertainty is associated with each forecast. For this reason, point forecasts can be of almost no value without the accompanying prediction intervals.

-- from Hyndman & Athanasopoulos (2018) OTexts

I have read the definition of predict confidence interval from the book, but I still not sure about the value outside the confidence interval. Can I say it is a warning signal or structure change?

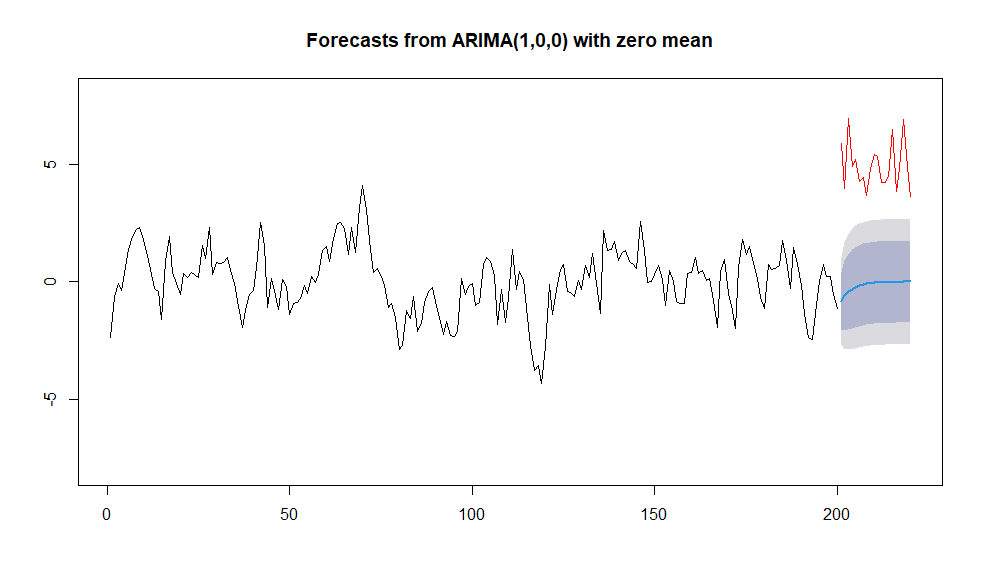

The example below

set.seed(123)

ts.sim <- arima.sim(list(order = c(1,0,0), ar = 0.8), n = 200)

ts.plot(ts.sim)

model <- Arima(ts.sim,c(1,0,0),include.mean = FALSE,include.drift = FALSE,method = "ML")

plot(forecast(model,h=20),ylim=c(-8,8))

lines(c(rep(NA,200),5+rnorm(20,0,1)),type="l",col="red")

The red line are out of the 95% predict confidence interval.

Thanks for every help!