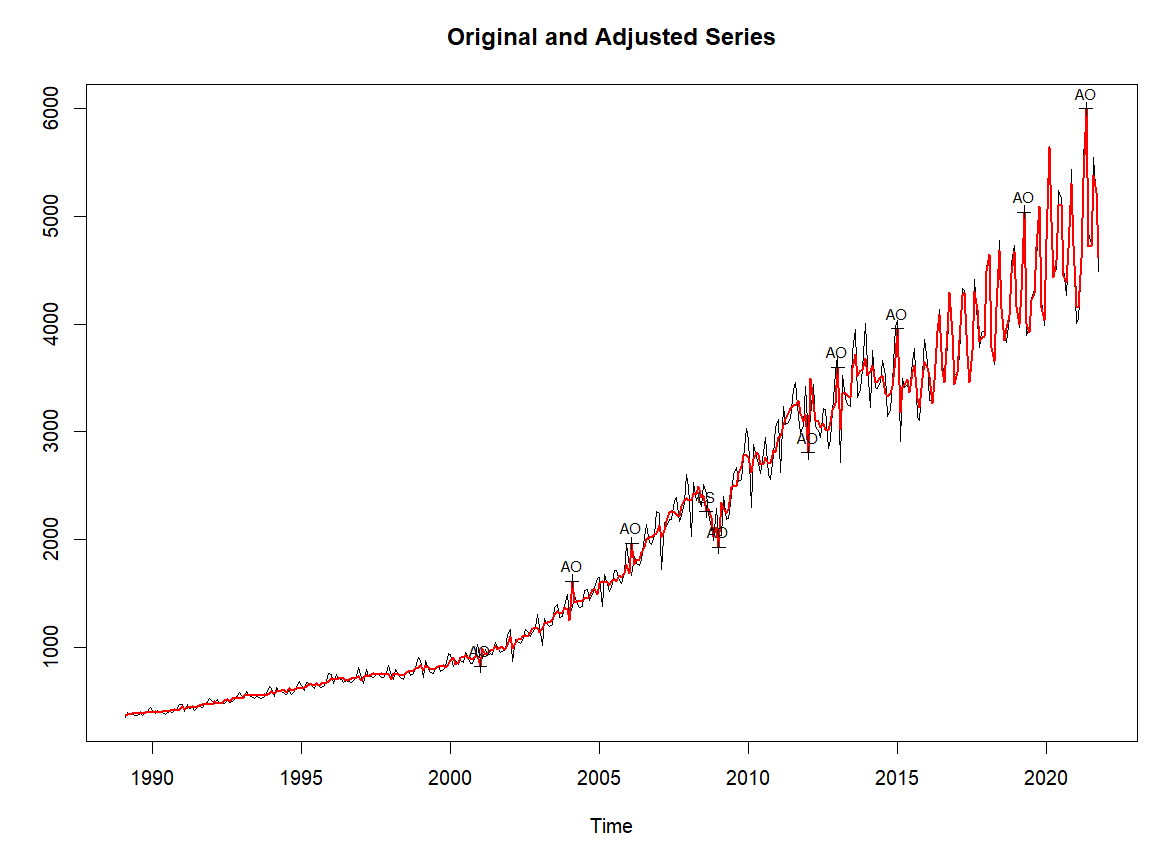

I am currently using the "seasonal" package in R to perform X-13ARIMA seasonal adjustment when I notice that the data I am analyzing have significantly larger volatility in recent years than in the past. As a result, the "seasonally-adjusted" time series does not remove the seasonality in those high-volatility years, as shown in the plot below:

I wonder if there is anything I can do to perform seasonal adjustment while taking heteroskedasticity into account at the same time (I've tried adding the parameter "transform.function = 'log'" when creating the seas object but to no avail)?