Field's Discovering Statistics Using SPSS (2013, Sage) defines sphericity as follows:

Sphericity: a less restrictive form of compound symmetry which assumes that the variances of the differences between data taken from the same participant (or other entity being tested) are equal. This assumption is most commonly found in repeated-measures ANOVA but applies only where there are more than two points of data from the same participant.

This definition doesn't mention anything about the covariances between difference scores needing to be equal. Is that because the definition is incomplete, or because the covariances don't need to be equal? Why is it necessary/not necessary for covariances to be equal?

I found here a comment stating that sphericity implies the difference variables should have the same covariances as each other:

Sphericity implies that "difference variables" (i.e. with 3 RM levels these are: RM1-RM2, RM1-RM3, RM2-RM3) have the identity covariance matrix

I'm thinking here about a repeated-subjects ANOVA.

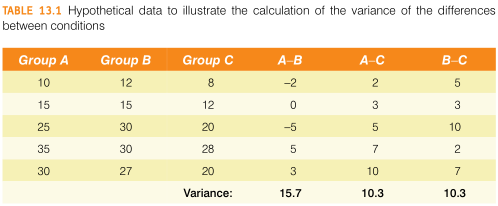

Here is a table from Field (2013) that illustrates what I mean by difference scores.

As noticed in the comments, there is an error in the book. I've assumed that the first value in Group C is really 8, and that therefore B-C should be 4, and Variance B-C should be 10.7.

I have calculated the covariances between the difference scores (not the actual scores) and they are as follows:

A-B, A-C 7.65

A-B, B-C -8.05

A-C, B-C 2.65

It turns out that the variances of the difference scores are a bit dissimilar (15.7, 10.3, 10.7). However, let's imagine those variances were exactly the same as each other (15.7, 15.7, 15.7), but the three covariances remained very different from one another. Would sphericity thereby be violated? Or are the covariances between difference scores not relevant to sphericity? Why are they relevant or not relevant to sphericity?