How to sample from a given univariate CDF is a huge subject, so I will assume that part of the answer is known and will address how to find the conditional CDF from the copula.

By definition, any copula assigns probabilities to rectangular regions (within the unit square) delimited on the right by its first argument and above by its second argument. In particular, when $U$ and $V$ are uniformly distributed with $C$ as the copula for $(U,V)$ and $0 \le \epsilon \lt 1 - u$$0 \lt \epsilon \le 1 - u$ is sufficiently small,

$$\eqalign{ \Pr(U\in (u, u+\epsilon)\text{ and }V \le v) &= \Pr(U\le u+\epsilon, V \le v) - \Pr(U\le u, V \le v) \\ &=C(u+\epsilon, v) - C(u, v). }$$$$\eqalign{ \Pr(U\in (u, u+\epsilon]\text{ and }V \le v) &= \Pr(U\le u+\epsilon, V \le v) - \Pr(U\le u, V \le v) \\ &=C(u+\epsilon, v) - C(u, v). }$$

Therefore, the conditional cumulative distribution function ought to arise as the (right-hand) limiting value of

$$\Pr(U\in (u, u+\epsilon)\text{ and }V \le v\,\Big|\,U\in (u, u+\epsilon)) = \frac{C(u+\epsilon, v) - C(u, v)}{\epsilon}.$$$$\Pr(U\in (u, u+\epsilon]\text{ and }V \le v\,\Big|\,U\in (u, u+\epsilon]) = \frac{C(u+\epsilon, v) - C(u, v)}{\epsilon}.$$

Provided this limit exists (which it will almost everywhere for $u$), by definition it is the first partial derivative, $\partial C(u,v)/\partial u$. This, therefore, gives the conditional CDF for $V\,\Big|\, U=u$ evaluated at $v$.

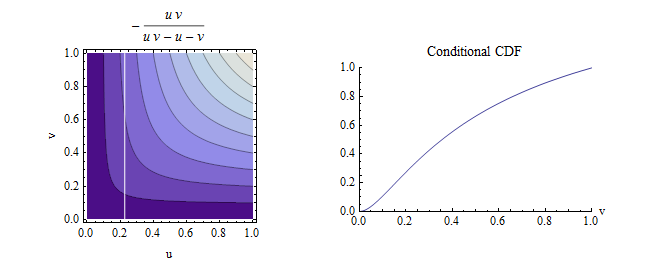

The left figure shows a contour plot of the copula (representing a surface) $C(u,v)=uv/(u+v-uv)$. The right figure is the graph of the conditional distribution of $V$ for $u\approx 0.23$. It is a cross section of the rightward slope of the surface.

###Reference###

Roger B. Nelsen, An Introduction to Copulas, Second Edition. Springer 2006: Section 2.9, Random Variate Generation.