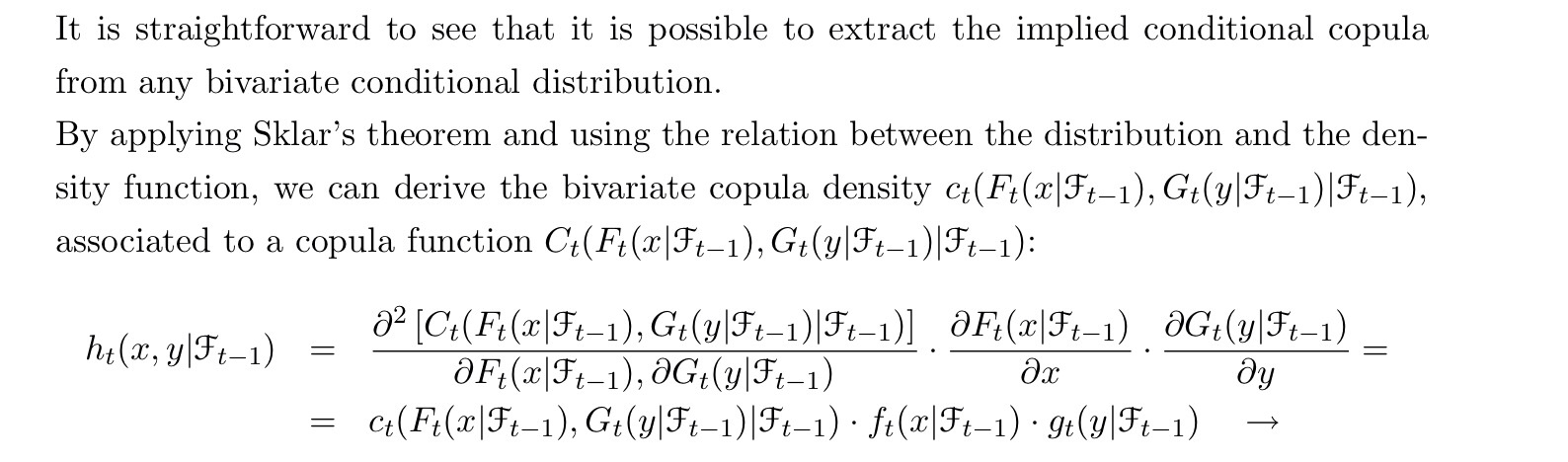

In the equation h_t(x,y|...) = ....$h_t(x,y|...) = ...$, can anyone explain me why the first derivatives of the marginal distributions are included? H_t$H_t$ is a distribution function and h_t$h_t$ its density function.

![Distribution function][1]

![Distribution function][1]

![Copula density][2]

![Copula density][2]

Using the relation between distribution and density function I can't get it to make sense.