Thanks to atireto's comment, I realized that I haven't taken into account the covariances between the estimated parameters. I was assuming that a and b are uncorrelated random variables, but they are not. So I corrected the sampling of a and b by converting them to correlated random variables using Cholesky decomposition of variance-covariance matrix (see heresee here).

replaced http://stats.stackexchange.com/ with https://stats.stackexchange.com/

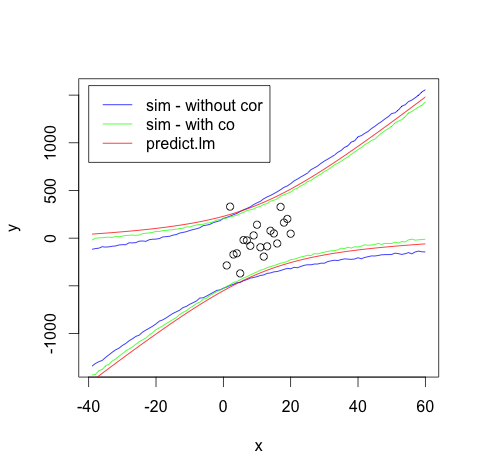

Thanks to atireto's comment, I realized that I haven't taken into account the covariances between the estimated parameters. I was assuming that a and b are uncorrelated random variables, but they are not. So I corrected the sampling of a and b by converting them to correlated random variables using Cholesky decomposition of variance-covariance matrix (see here).

Here's the corrected code:

rm(list = ls())

n = 20 # number of points

N = 10000 # simulation rounds

x = 1:n # x

s = 200 # standard deviation of error

set.seed(12)

e = rnorm(n, 0, s)

a = 5; b = 5 # slope, intercept

y = a * x + b + e

## lm model

mod1 = lm(y ~ x)

summ_mod1 = summary(mod1)

## std errors

coefs = summ_mod1$coefficients[, 1:2]

sigma = summ_mod1$sigma

## predict new data using simulation

new.x = (min(x) - 2 * max(x)):(max(x) + 2 * max(x))

upper = rep(0, length(new.x))

lower = rep(0, length(new.x))

tmp = rep(0, N)

for (i in 1:length(new.x)) {

tmp = rnorm(n = N, mean = coefs[1, 1], sd = coefs[1, 2]) +

rnorm(n = N, mean = coefs[2, 1], sd = coefs[2, 2]) * new.x[i] +

rnorm(n = N, mean = 0, sd = sigma)

upper[i] = mean(tmp) + 1.96 * sd(tmp)

lower[i] = mean(tmp) - 1.96 * sd(tmp)

}

plot(x, y, type = "p",

xlim = c(min(new.x), max(new.x)),

ylim = c(min(lower), max(upper)))

lines(new.x, lower, col = "blue")

lines(new.x, upper, col = "blue")

## R's prediction interval

pred.int = predict(object = mod1,

newdata = data.frame(x = new.x),

interval = "predict",

level = 0.95)

pred.lower = pred.int[,2]

pred.upper = pred.int[,3]

lines(new.x, pred.lower, col = "red")

lines(new.x, pred.upper, col = "red")

## taking the variance-covariance matrix into account

L = chol(vcov(mod1))

for (i in 1:length(new.x)) {

beta = matrix(c(rnorm(n = N),

rnorm(n = N)),

nrow = 2)

beta_cor = t(L) %*% beta

tmp = coefs[1, 1] + beta_cor[1, ] +

(coefs[2, 1] + beta_cor[2, ]) * new.x[i] +

rnorm(n = N, mean = 0, sd = sigma)

upper[i] = mean(tmp) + 1.96 * sd(tmp)

lower[i] = mean(tmp) - 1.96 * sd(tmp)

}

lines(new.x, lower, col = "green")

lines(new.x, upper, col = "green")

legend(x = -40, y = 1600,

legend = c("sim - without cor", "sim - with co", "predict.lm"),

lty = c(1, 1, 1),

col = c("blue", "green", "red"))

It still doesn't perfectly match the R's predict.lm result, but it's very close. In fact, if I change the 1.96 coefficient to something like 2.1, it matches it perfectly. Predict.lm is supposed to be 95% prediction interval, so I'm not sure this is happening.