I am new to both ARIMA technique and R. Your suggesitonsuggestions would be very much appreciated.

I am dealing with hourly data with strong seasonality and have used auto.arimaauto.arima to select a model:

Fit<-auto.arima(H_ts, seasonal=TRUE ,approximation=FALSE)

This is the model it returns: ARIMA(5,1,4)(1,0,0)[24]

Coefficients:

ar1 ar2 ar3 ar4 ar5 ma1 ma2 ma3 ma4 sar1

0.6361 0.4046 0.5212 -0.7154 -0.0334 -0.5638 -0.4464 -0.5704 0.6325 0.0917

s.e. 0.0977 0.1390 0.1109 0.0968 0.0181 0.0957 0.1282 0.1152 0.0821 0.0114

sigma^2 estimated as 14.24: log likelihood=-12188.98

AIC=24399.96 AICc=24400.02 BIC=24470.34

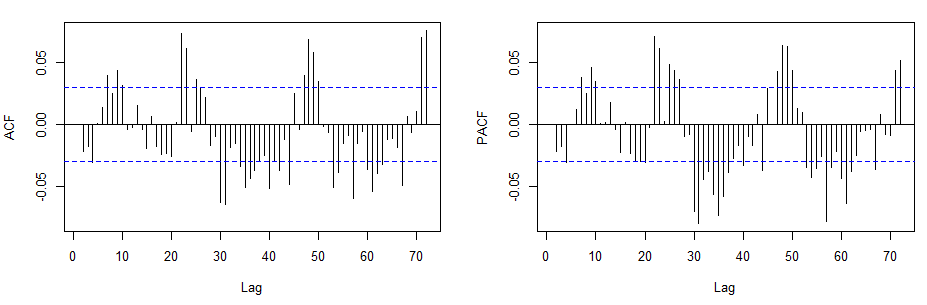

However, the residualsresidual ACF and PACF look quite suspicious:

Any idea what I can do to 'fix' this?