UPDATE :

So, I tried a few different things and this is what I learnt:

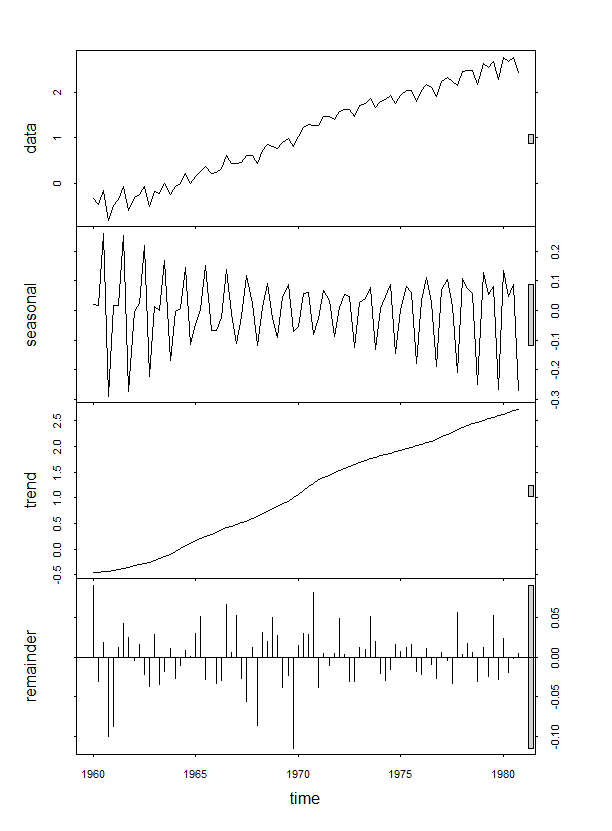

a) In order to fit the trend, I can first extract the trend time series generated by the stl() function in R and then perform fitting on it as follows:

> Trend=decomp_JJ$time.series[,2]

> t=time(decomp_JJ$time.series[,2])

> fit_Trend=lm(Trend~0+t)

> summary(fit_Trend)

Call:

lm(formula = Trend ~ 0 + t)

Residuals:

Min 1Q Median 3Q Max

-1.55503 -0.90810 0.07018 0.87686 1.60349

Coefficients:

Estimate Std. Error t value Pr(>|t|)

t 5.628e-04 5.648e-05 9.965 7.72e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 1.02 on 83 degrees of freedom

Multiple R-squared: 0.5447, Adjusted R-squared: 0.5392

F-statistic: 99.3 on 1 and 83 DF, p-value: 7.723e-16

but I am not sure, if this is the correct way to proceed. Also, I haven't still figured out how to fit the seasonal component