I am very new to Time Series Analysis (together with R). I have been practising with some very simple datasets to understand how to decompose the time series into Trend, Seasonal and Error components and then check whether the Error component is Gaussian or not. Till this point, everything is pretty much clear to me. However, after the decomposition, how do I fit the trend and seasonal component, using R that is? I am confused on 'to what' do I fit my trend and seasonal component? I mean what should my predictors be? Time, perhaps?

Below is one of time series datsets that I used. This time series is called 'jj' and is present in the 'astsa' package. The frequency of this time series is quarterly.:

> jj

Qtr1 Qtr2 Qtr3 Qtr4

1960 0.710000 0.630000 0.850000 0.440000

1961 0.610000 0.690000 0.920000 0.550000

1962 0.720000 0.770000 0.920000 0.600000

1963 0.830000 0.800000 1.000000 0.770000

1964 0.920000 1.000000 1.240000 1.000000

1965 1.160000 1.300000 1.450000 1.250000

1966 1.260000 1.380000 1.860000 1.560000

1967 1.530000 1.590000 1.830000 1.860000

1968 1.530000 2.070000 2.340000 2.250000

1969 2.160000 2.430000 2.700000 2.250000

1970 2.790000 3.420000 3.690000 3.600000

1971 3.600000 4.320000 4.320000 4.050000

1972 4.860000 5.040000 5.040000 4.410000

1973 5.580000 5.850000 6.570000 5.310000

1974 6.030000 6.390000 6.930000 5.850000

1975 6.930000 7.740000 7.830000 6.120000

1976 7.740000 8.910000 8.280000 6.840000

1977 9.540000 10.260000 9.540000 8.729999

1978 11.880000 12.060000 12.150000 8.910000

1979 14.040000 12.960000 14.850000 9.990000

1980 16.200000 14.670000 16.020000 11.610000

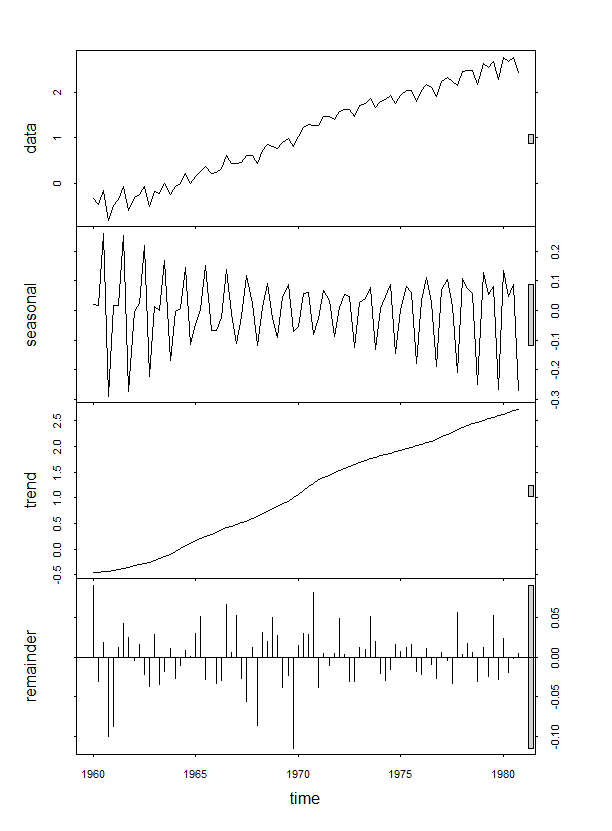

> decomp_JJ=stl(log(jj),s.window = 4)

> plot(decomp_JJ)

Any help on this is much appreciated!