company date hbVol wikiVol stockVol0 comp1 comp2 ... comp89 marketRet

-------------------------------------------------------------------------------

1 1 200 150 2423325 1 0 ... 0 -2.50

1 2 194 152 2455343 1 0 ... 0 -1.45

. . . . . . . ... .

1 103 205 103 2563463 1 0 ... 0 1.90

2 1 752 932 7434124 0 1 ... 0 -2.50

2 2 932 823 7464354 0 1 ... 0 -1.45

. . . . . . . ... .

. . . . . . . ... .

86 103 3 55 32324 0 0 ... 1 1.90

How to perform pooled cross-sectional time series analysis?

For 86 companies and for 103 days, I have collected (i) tweets (variable hbVol) about each company and (ii) pageviews for the corporate wikipedia page (wikiVol). The dependent variable is each company's stock trading volume (stockVol0). My data is structured as follows:

company date hbVol wikiVol stockVol0

------------------------------------------------

1 1 200 150 2423325

1 2 194 152 2455343

. . . . .

1 103 205 103 2563463

2 1 752 932 7434124

2 2 932 823 7464354

. . . . .

. . . . .

86 103 3 55 32324

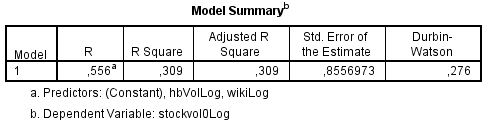

As I understood, this is called pooled cross-sectional time series data. I have taken the Log-value of all variables to smoothen the big differences between companies. A regression model with both independent variables on the dependent stockVolo returns:

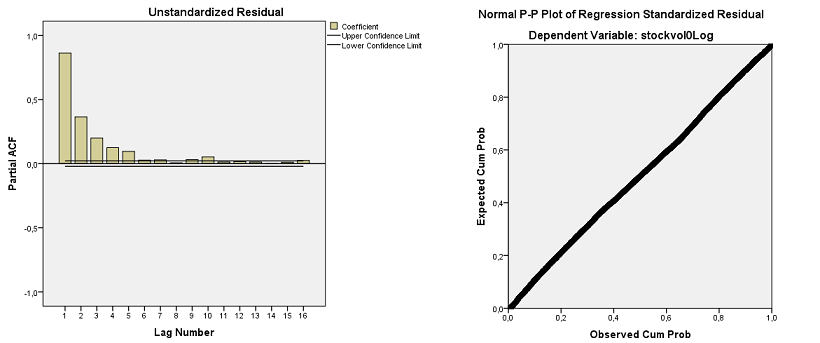

A Durbin-Watson of 0,276 suggest significant autocorrelation of the residuals. The residuals are, however, bellshaped, as can be seen from the P-P plot below. The partial autocorrelation function shows a significant spike at a lag of 1 to 5 (above upper limit), confirming the conclusions drawn from the Durbin-Watson statistic:

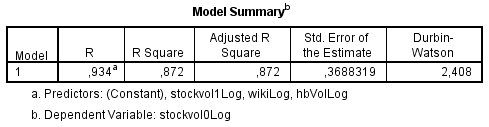

The presence of first-order autocorrelated residuals violates the assumption of uncorrelated residuals that underlies the OLS regression method. Different methods have been developed, however, to handle such series. One method I read about is to include a lagged dependent variable as an independent variable. So I created a lagged stockVol1 and added it to the model:

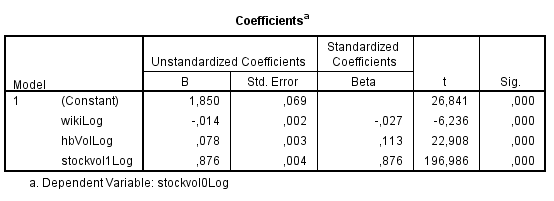

Now, Durbin-Watson is at an accceptable 2,408. But obviously, R-squared is extremely high because of the lagged variable, see also the coefficients below:

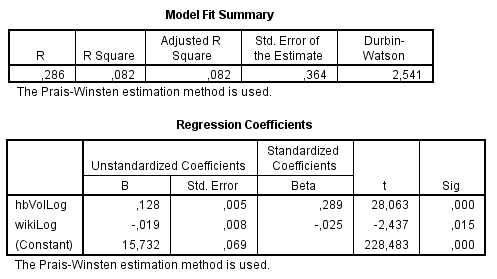

Another method I read about when being confronted with autocorrelation, is autoregression with Prais-Winsten (or Cochrane-Orcutt) method. Once performing this the model reads:

This is what I don't understand. Two different methods, and I get very different results. Other suggestions for analyzing this data include (i) not including a lagged variable but reformat the dependent variable by differencing (ii) perform AR(1) or ARIMA(1,0,0) models. I haven't calculated those because I am now lost on how to proceed because of the different results of the two tests I did perform.

What model should I use to perform a proper regression on my data? I'm very keen on understanding this, but have never had to analyze a timeseries dataset like this before.