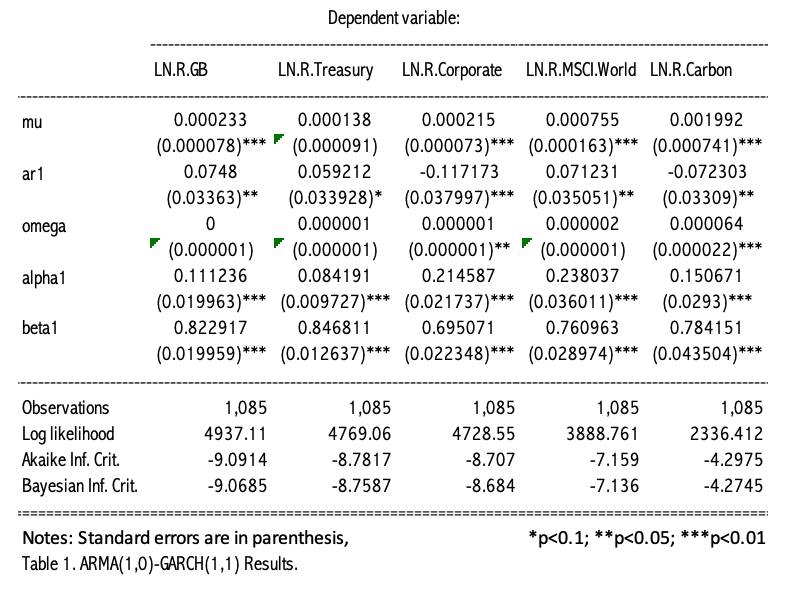

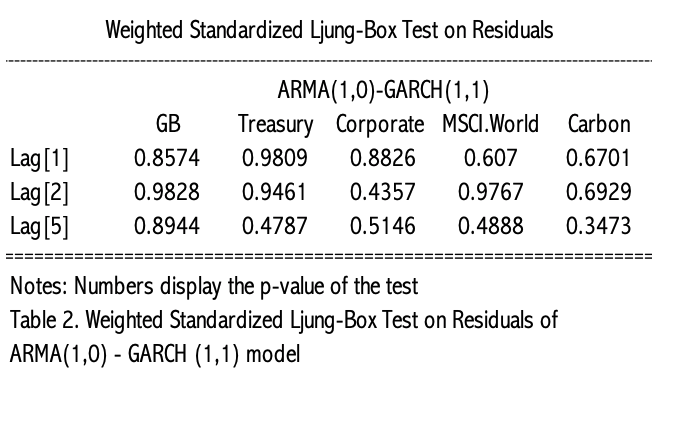

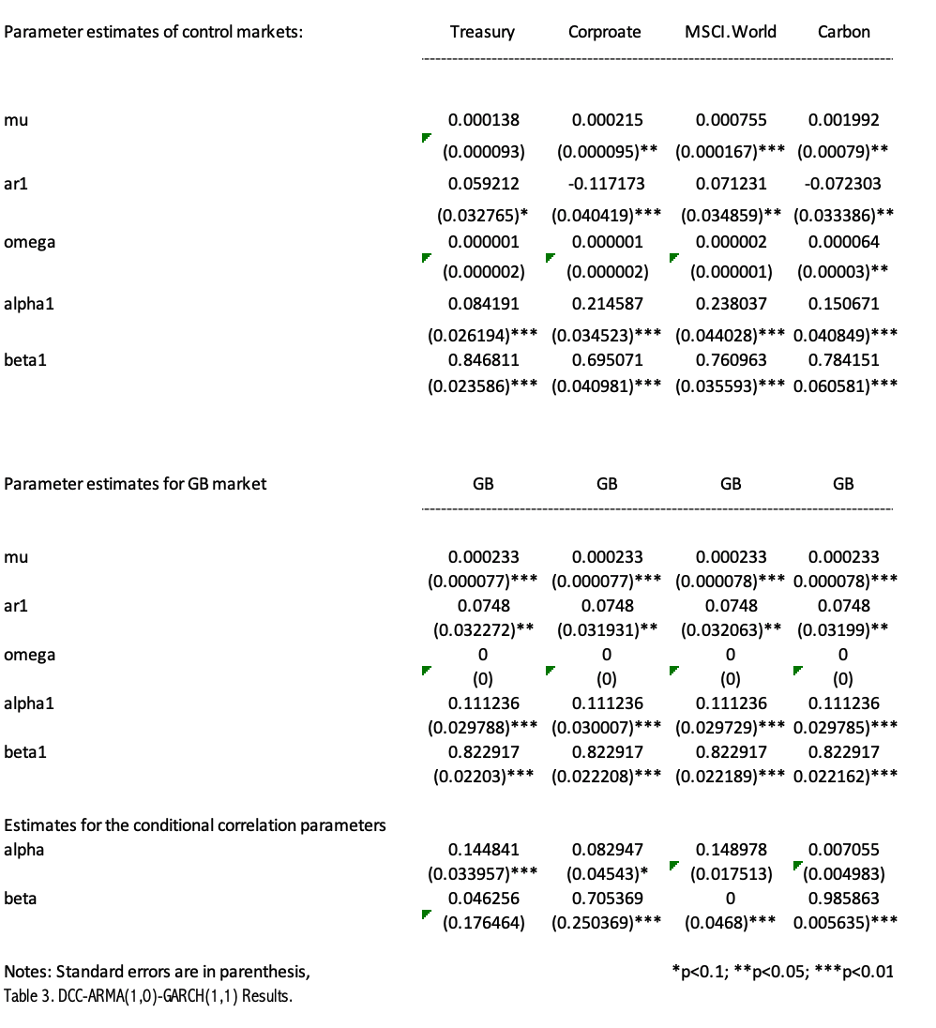

I'm using a DCC-ARMA(1,0)-GARCH(1,1) model to investigate co-movement of the green bond market and other markets. The ARCH/GARCH parameters of the univariate ARMA(1,0)-GARCH(1,1)models are significant (see table 1) and the Ljung-Box test of their wieghted standardized residuals indicates that the univariate model is sufficent in modelling the respective markets conditional variance (see table 2). Based on this, the univariate model seems fine. However, neither market has both dccalpha and dccbeta as significant with that of the GB market(see table 3). Does this mean that DCC-model I am using is insufficient in modellin the markets co-movement?