I've run a path analysis using semTools. I'm interested to test indirect effects. The p values for all indirect effects were non-significant, but the Monte Carlo confidence interval for some of them did not contain zero.

My question is - is it appropriate to use only Monte Carlo confidence interval, but not p-values to report and interpret the results?

I did some search online but I'm afraid there was limited info. I saw this post: Non-significant p-values but CI does not include 0, but the answer talked about bootstrapping. In my study, I used multiple imputations to handle missing data, so bootstrapping was not appropriate.

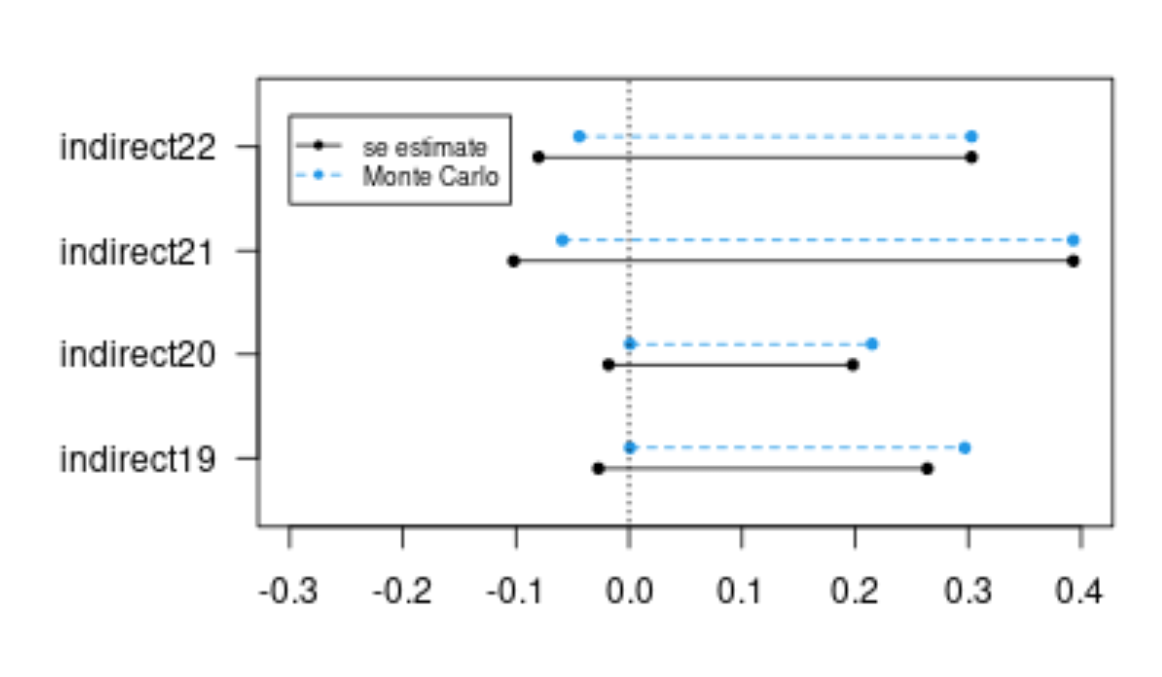

Below are some codes showing the conflicting results. Because the codes for my model is long, I didn't show it below. I've shown the codes that are relevant to my question. Indirect effect 19 and 20 below had non-significant p values, but the Monte Carlo CI did not contain zero.

I saw some people saying that they would not trust the p-values because they are computed assuming the Z-statistic comes from a standard normal distribution (thus potentially favouring Monte Carlo CI). But I also saw some people saying that the p values and CI (not specific to Monte Carlo though) should be consistent with each other. If they are not consistent, I should not reject the null hypothesis. Can anyone please shed some light on this?

output <- runMI(model, data=data3c.mi.1, fun="sem", estimator = "MLR", se = "robust.huber.white")

Estimate Std.Err t-value df P(>|t|) ci.lower ci.upper Std.lv Std.all

indirect19 0.118 0.074 1.593 1563.011 0.111 -0.027 0.264 0.119 0.008

indirect20 0.090 0.055 1.639 1924.600 0.101 -0.018 0.198 0.091 0.009

indirect21 0.146 0.126 1.152 714.059 0.250 -0.102 0.393 0.147 0.010

indirect22 0.112 0.097 1.147 664.112 0.252 -0.080 0.303 0.112 0.011

monteCarloCI(output, standardized = TRUE)

est ci.lower ci.upper

indirect19 0.119 0.001 0.297

indirect20 0.091 0.001 0.215

indirect21 0.147 -0.059 0.393

indirect22 0.112 -0.044 0.303