If your primary concern is to use the ACF and PACF plots to guide a good ARMA fit then http://people.duke.edu/~rnau/411arim3.htm is a good resource. In general, AR orders will tend to present themselves by a sharp cutoff in the PACF plot and a slow trending or sinusoidal degradation in the ACF plot. The opposite is usually true for MA orders...the link provided above discusses this in more detail.

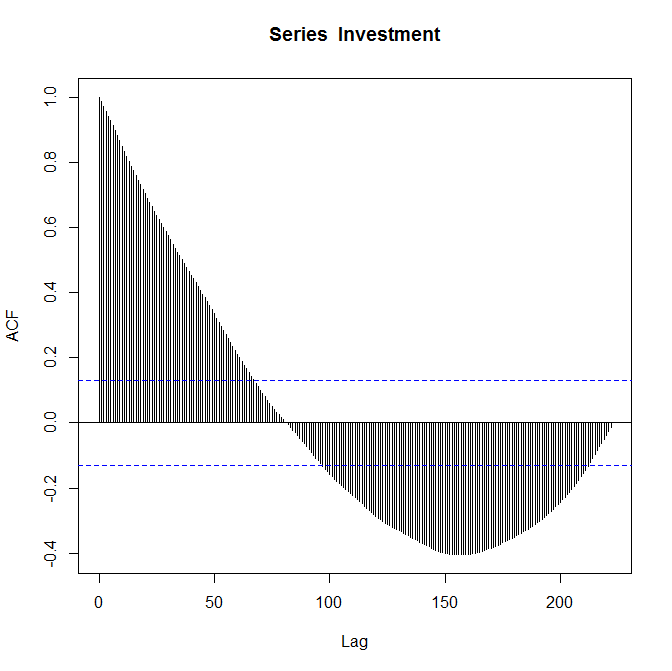

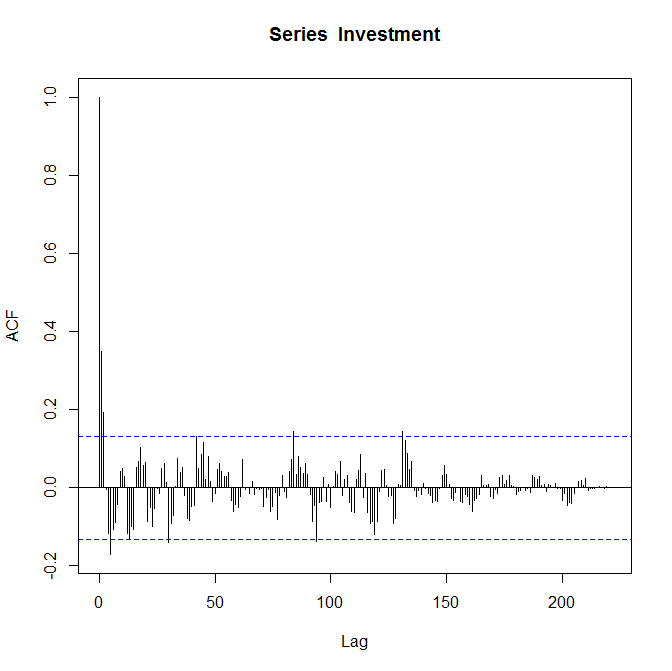

The ACF plot you provided may suggest an MA(2). I would guess that you have some significant AR orders just looking at the sinusoidal decay in auto-correlation. But all this is extremely speculative since the coefficients become insignificant very quickly as lag increases. Seeing the PACF would be very helpful.

Another important thing you want to watch for is significance in the 4th lag on the PACF. Since you have quarterly data, significance in the 4th lag is a sign of seasonality. For example if your investment is a gift store, returns may higher during the holidays (Q4) and lower during the beginning of the year (Q1), causing correlation between identical quarters.

The significant coefficients for smaller lags in the ACF plot should stay the same as your data size increases assuming nothing changes with the investment. Higher lags are estimated with less data points then are lower lags (i.e every lag looses a data point), so you can use the sample size in the estimation of each lag to guide your judgment as to which will stay the same and which are less reliable.

Using the ACF plot to make deeper insights about your data (beyond just an ARMA fit) would require a deeper understanding of what type of investment this is. I have commented on this already.

For deeper insight...

With financial assets, practitioners often log then difference price to obtain stationary. The log

difference is analogous to a continually compacted returns (i.e. growth) so it

has a very nice interpretation and there is a lot of financial literature available

on studying/modeling series of asset returns. I assume your stationary data was obtained in this manner.

In the most general sense, I would say the auto-correlation means that returns on the investment are somewhat predictable. You could use an ARMA fit to forecast future returns or comment on the investment's performance when compared to a benchmark such as the S&P 500.

Looking at the variance in residual terms of the fit also gives you a measure of risk in the investment. This is extremely important. In finance you want an optimal risk to return trade off

and you can decide if this investment is worth the money by comparing to other market benchmarks. For example, if these returns have a low mean

and are hard to predict (i.e risky) when compared to other investment options, you would know its a bad investment. Some good places to start are

http://en.wikipedia.org/wiki/Efficient_frontier and http://en.wikipedia.org/wiki/Modern_portfolio_theory.

Hopefully that helps!