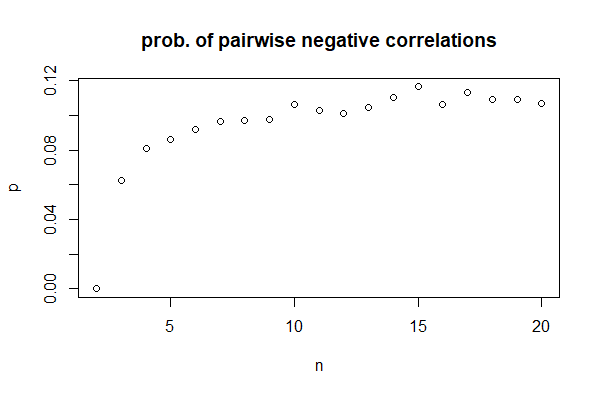

It is possible if the size of the vector is 3 or larger. For example

\begin{align}

a &= (-1, 1, 1)\\

b &= (1, -9, -3)\\

c &= (2, 3, -1)\\

\end{align}

The correlations are

\begin{equation}

\text{cor}(a,b) = -0.80...\\

\text{cor}(a,c) = -0.27...\\

\text{cor}(b,c) = -0.34...

\end{equation}

We can prove that for vectors of size 2 this is not possible:

\begin{align}

\text{cor}(a,b) &< 0\\[5pt]

2\Big(\sum_i a_i b_i\Big) - \Big(\sum_i a_i\Big)\Big(\sum_i b_i\Big) &< 0\\[5pt]

2(a_1 b_1 + a_2 b_2) - (a_1 + a_2)(b_1 b_2) &< 0\\[5pt]

2(a_1 b_1 + a_2 b_2) - (a_1 + a_2)(b_1 b_2) &< 0\\[5pt]

2(a_1 b_1 + a_2 b_2) - a_1 b_1 + a_1 b_2 + a_2 b_1 + a_2 b_2 &< 0\\[5pt]

a_1 b_1 + a_2 b_2 - a_1 b_2 + a_2 b_1 &< 0\\[5pt]

a_1 (b_1-b_2) + a_2 (b_2-b_1) &< 0\\[5pt]

(a_1-a_2)(b_1-b_2) &< 0

\end{align}

The formula makes sense: if $a_1$ is larger than $a_2$, $b_2$ has to be larger than $b_1$ to make the correlation negative.

Similarly for correlations between (a,c) and (b,c) we get

\begin{equation}

(a_1-a_2)(c_1-c_2) < 0\\

(b_1-b_2)(c_1-c_2) < 0\\

\end{equation}

Clearly, all of these three formulas can not hold at the same time.