Consider a linear regression model y on x and x on y. We have

$Y = a'X + a$ where $a' = \frac{cov(X,Y)}{Var(X)}$. Equivalently, we have $X = b'Y+b$ where $b' = \frac{cov(X,Y)}{Var(Y)}$. I am interested in the relationship between $a'$ and $b'$

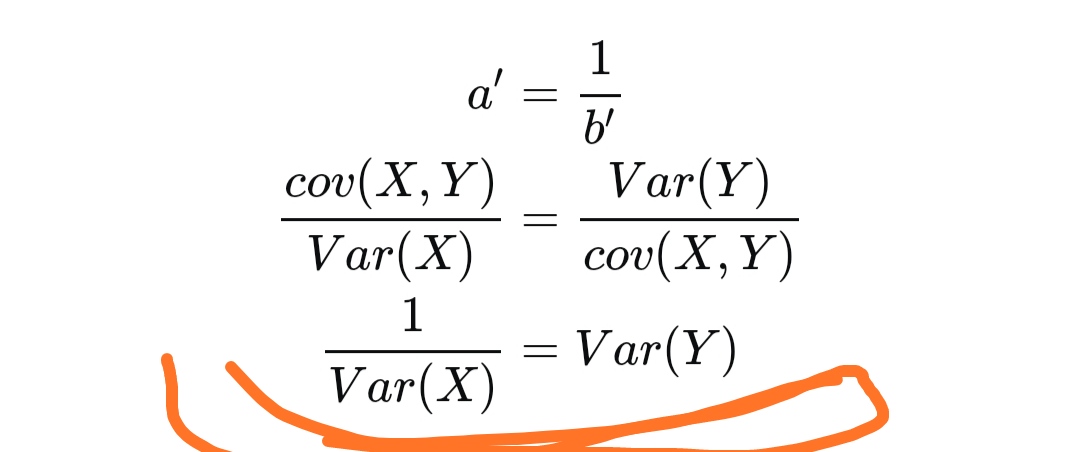

Clearly, if $Var(X) = Var(Y)$ then we have $a'=b'$. However, say we want $a' = \frac{1}{b'}$. It follows that:

\begin{aligned} a' &= \frac{1}{b'} \\ \frac{cov(X,Y)}{Var(X)} &= \frac{Var(Y)}{cov(X,Y)} \\ \frac{1}{Var(X)} &= Var(Y) \end{aligned}

Ok. What about this example then, where

\begin{aligned} y &= 2x \\ \frac{1}{2}y &= x \\ &\text{but} \\ Var(Y) &= 4Var(X) \\ \end{aligned}

Clearly we have $a' = \frac{1}{b'}$ but our variances are not inverses of one another. Where is my understanding faulty?