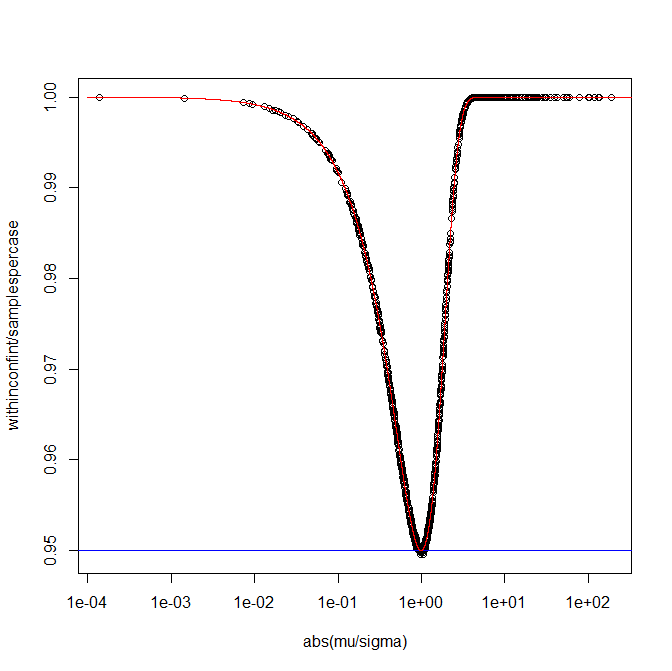

Here is a simulation to demonstrate that @soakley's confidence interval works for a normally distributed random variable.

- It takes $10^4$ values of $\mu$ in $[-10,10]$ and of $\sigma$ in $[0,10]$ and

- for each of those pairs, it generates $10^6$ single observations $x$ and

- sees what proportion of the corresponding confidence intervals $[x- 9.68|x|, x+9.68|x|]$ cover $\mu$.

- It then plots this proportion against $\frac{|\mu|}{\sigma}$ as small black circles to illustrate when this proportion is about $0.95$ (the blue line) and when it is much higher.

- The red line shows the theoretical confidence for varying values of $\frac{|\mu|}{\sigma}$.

Using R:

set.seed(2023)

cases <- 10^3

samplespercase <- 10^6

mu <- runif(cases)*20-10

sigma <- runif(cases)*10

withinconfint <- numeric(cases)

for (i in 1:cases){

sample <- rnorm(samplespercase, mean=mu[i], sd=sigma[i])

withinconfint[i] <- sum(sample - 9.68*abs(sample) < mu[i] &

sample + 9.68*abs(sample) > mu[i])

}

plot(abs(mu/sigma), withinconfint/samplespercase, log="x")

abline(h=0.95,col="blue")

curve(pnorm(x/(1-9.68),x,1) + 1 - pnorm(x/(1+9.68),x,1),

from=10^-4, to=10^4, col="red", n=50001, log="x", add=TRUE)

Taking account of simulation noise, this suggests the claim and the corresponding expression for theoretical confidence of $\Phi\left(\frac{9.68}{(1-9.68)x}\right) + 1 - \Phi\left(\frac{-9.68}{(1+9.68)x}\right)$ are highly plausible. When $\frac{|\mu|}{\sigma} \approx 1$ the confidence is marginally above $0.95$, though at other times it is much more conservative and closer to $1$.

The chart seems to suggest the minimum confidence is when $\frac{|\mu|}{\sigma} = 1$; this is not quite correct and for $\alpha=1-0.95=0.05$ it is closer to $0.99$; for larger $\alpha < \frac12$ it would be at an even lower value of $\frac{|\mu|}{\sigma}$.

Meanwhile the $9.68$ is marginally higher than $\sqrt{\frac{2}{e\pi}} /\alpha \approx \frac{0.48394}{\alpha}$ and needs to be. For all $\alpha < \frac12$ we can use the slightly more conservative $\frac{0.5}{\alpha}$ and so a confidence interval of $\left[x-\frac1{2\alpha}|x|, x+\frac1{2\alpha}|x|\right]$ to have a probability of over $1-\alpha$ of covering the unknown mean, which in this example would have been $x\pm 10|x|$ which would have given confidence of about $0.9516$ in the tightest case.