I'm reading through Fan and Li (2001) Variable Selection via Nonconcave Penalized Likelihood and its Oracle Properties. On p. 1349 (near the bottom-right corner) they proposed three properties that a good penalized estimator should have:

- Unbiasedness: The resulting estimator is nearly unbiased when the true unknown parameter is large to avoid unnecessary modeling bias.

- Sparsity: The resulting estimator is a thresholding rule, which automatically sets small estimated coefficient to zero to reduce model complexity.

- Continuity:The resulting estimator is continuous in data z to avoid instability in model prediction.

They then showed that the hard thresholding penalty function can result in estimators with those good properties, given some conditions satisfied. Specifically,

- (1) A sufficient condition for unbiasedness is $p_\lambda'(\theta)=0$ for large $|z|$;

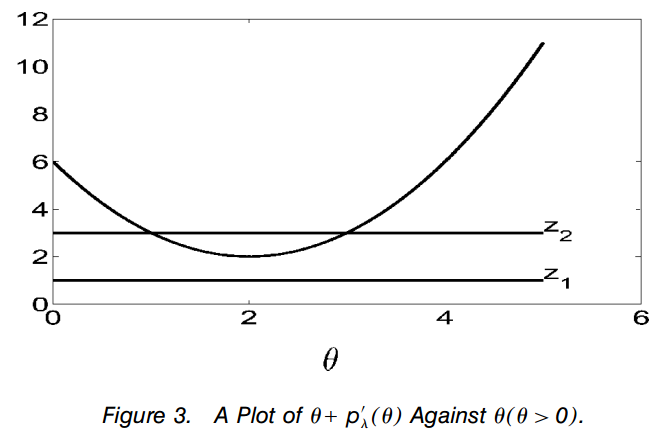

- (2) A sufficient condition for sparsity is $\text{min}_{\theta \neq 0} \{|\theta| + p_\lambda'(\theta)\} \gt 0$;

- (3) A sufficient and necessary condition for continuity is that the minimum of the function $|\theta| + p_\lambda'(\theta)$ is attained at 0.

My questions are:

- For proving condition (2), they depicted a figure below. I am confused why $\theta + p_\lambda'(\theta)$ is a Parabola since it is equal to $\theta + 2(\lambda - \theta)I(\theta < \lambda)$. And moreover, how does the proof to condition (2) come from this figure?

Update: Figure 3 should be a general illustration about $\theta + p_\lambda'(\theta)$ against $\theta (>0)$, as pointed out by @Glen_b.

- The last sentence of first paragraph in Page 3 concludes that "a penalty function satisfying the conditions of sparsity and continuity must be singular at the origin". Why is that?

Obviously I totally missed the points here. Could any of you walk me through the arguments made for proving conditions (2) and (3)? Thank you very much for the help.