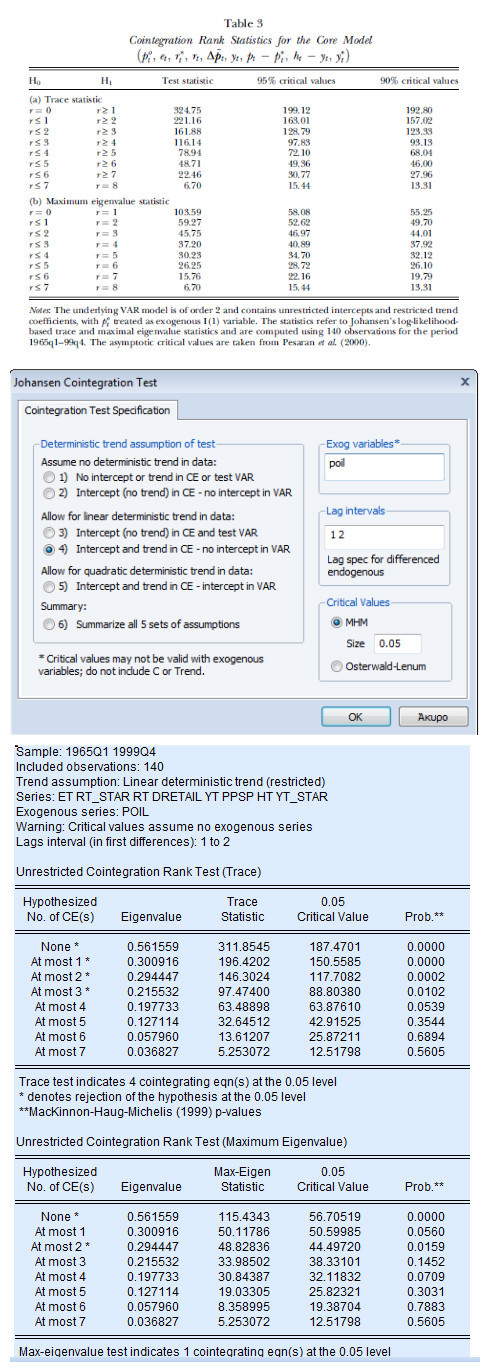

I am trying to replicate Tables 3 and 4 from the paper "A Long Run Structural Macroeconometric Model OF the UK" by Garratt et al (2003).

Using the Akaike criterion the authors decide to proceed with a VAR(2) model with unrestricted intercepts and restricted trend coefficients (this is option IV on the Eviews programme I reckon). The VAR consists of 9 variables, these are ($p_t^{oil}$, $e_t$, $r_t^*$, $r_t$, $\Delta Retail.price.index_t$, $y_t$, $p_t-p_t^*$, $h_t-y_t$, $y_t^*$) with $p_t^{oil}$ treated as an exogenous I(1) variable.

The authors found 5 and 2 cointegrating relationships using the Trace and Maximum Eigen Value tests respectively. They proceed assuming 5 cointegrating relationships. My findings suggest 4 cointegrating relationships for the former test and 1 for the latter. How can I replicate the author's findings?

The actual table 3 from Garratt et al. (2003) paper, my first step using Eviews and my conflicting results follow below.

Please find to this link my incomplete EViews Programme.