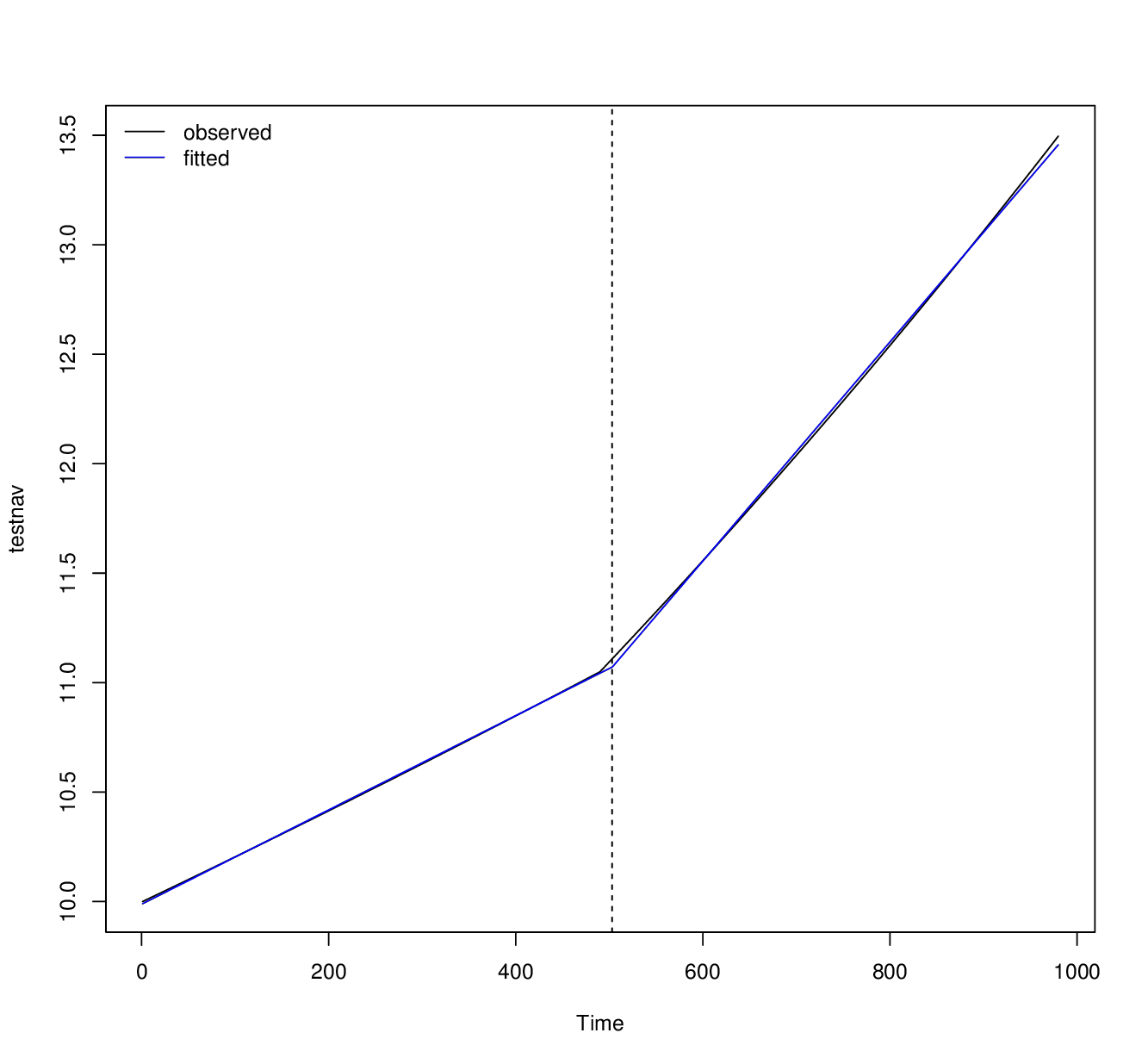

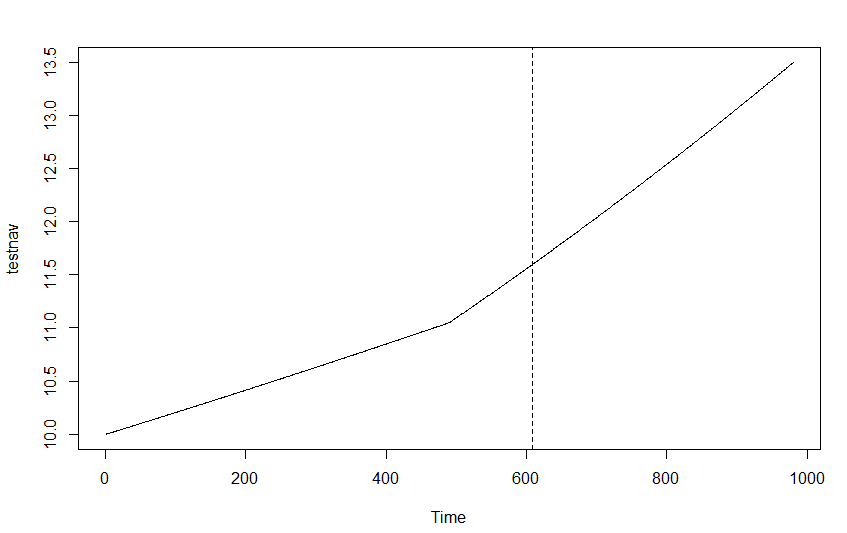

I'm trying to detect structural breaks in time series of NAV using 'strucchange' in R.

I have created the NAV by using a simple annualized return of 5% and 10% (no random term). However, after using 'breakpoints' test in R the result is that the break point is not on the point I have changed return from 5% to 10%.

My code is like:

library(readr)

test <- read_csv("D:/Temp/Test/nav.csv")

View(test)

library(strucchange)

testnav = ts(test$NAV)

bp.test = breakpoints(testnav ~ 1)

plot(testnav)

lines(bp.test, breaks = 1)

The data I use is Here

Did I do something wrong? Why isn't it break on time ~500 where the return changed from 5% to 10%?