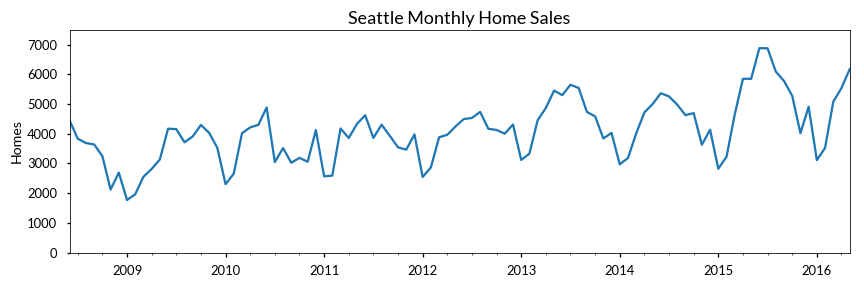

I'm writing a blog post on forecasting time series with autoregression. In it, I compare the performance of SLR, ARIMA, and SARIMAX on forecasting the number of Home Sales in Seattle (see below).

All 3 have different numbers of "input parameters": SLR just uses time, ARIMA and SARIMAX both use time and 12 lagged $y$ values. *I say "input parameters" b/c I'm not sure how to consider $y$.

I'm currently using RMSE to compare them. Is this an acceptable practice, or is there another measure I should use that takes model complexity into account (e.g. something akin to adjusted R^2)?

I know that MAPE is a commonly used forecasting metric. But like RMSE, I'm not sure it's appropriate for comparing models with different numbers of input parameters. Just wondering if there's anything better out there.