Suppose we have a random sample of size $n = 100$ from $\mathsf{Expo}(rate = \lambda = 0.02).$

Then the smallest observation has $V = X_{(1)} \sim \mathsf{Expo}(rate = n\lambda = 2)$

because

$$F_V(t) = P(V \le t) = 1 - P(V > t) = 1 - [P(X_i > t)]^n = 1 - (e^{-\lambda t})^n = 1 - e^{-n\lambda t},$$

for $ t > 0,$ is the CDF of $\mathsf{Expo}(rate = n\lambda).$ Also,

$\lambda V \sim \mathsf{Expo}(n).$

Now suppose $Y = X + \theta$ with $Y_{(1)} = V + \theta = W.$ Then

$$P(L < \lambda V < U) = P(L/ \lambda < W - \theta < U /\lambda)\\=

P(W - U/\lambda < \theta < W - L/\lambda) = 0.95,$$

where $L = 0.00025$ and $U =0.0369,$ so that a 95% confidence interval for $\theta$ is

$(W - U/\lambda, W - U/\lambda).$

qexp(c(.025,.975), 100)

[1] 0.0002531781 0.0368887945

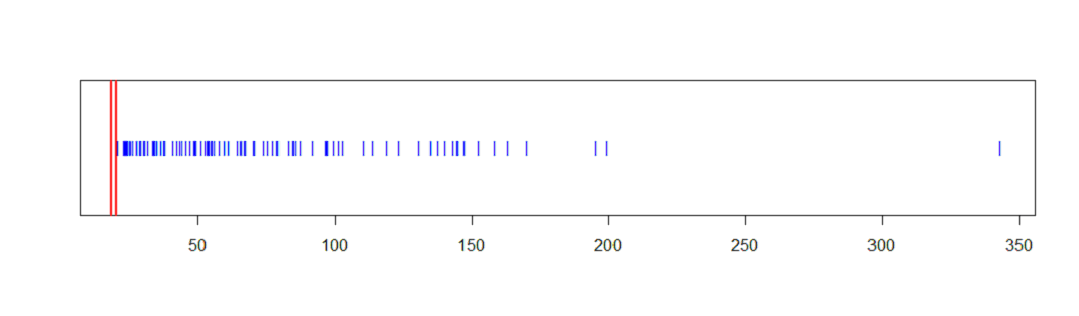

In particular, suppose $\lambda = 0.02,\, \theta = 20$ and we have the random sample $Y_1, Y_2, \dots, Y_{100}$ as generated in R below, with minimum $Y_{(1)} = 20.07.$

set.seed(920); n = 100; lam = .02; th = 20

y = rexp(n, lam) + th

w.obs = min(x); w.obs

[1] 20.07364

Then knowing that $\lambda = 0.02,$ we would have the 95% CI $(18.23, 20.06)$ for $\theta,$ shown as vertical red bars in the figure below.

w.obs - qexp(c(.975,.025), 100)/.02

[1] 18.22920 20.06098

stripchart(y, pch="|", col="blue")

abline(v=c(18.23,20.06), col="red", lwd=2)

The following simulation shows that this type of confidence interval covers the true value of $\theta$ for 95% of samples generated with the specified parameters.

set.seed(1234); n = 100; lam = .02; th = 20

w = replicate(10^5, min(rexp(n,lam)+th))

mean(w-qexp(.975, 100)/lam < th & w-qexp(.025, 100)/lam > th)

[1] 0.94984

Notes: (a) In the un-shifted case $(\theta = 0),$ Wikipedia

discusses estimation of the exponential rate $\lambda.$ While $\bar X$ is an unbiased estimator for the mean $\mu = 1/\lambda,$ The MLE for $\lambda$ is biased; an unbiased estimator of $\lambda$ is $(1-2/n)/\bar X.$ The Wikikpedia article discusses CIs for $\lambda.$

In particular, for the $n=100$ observations $X_i$ considered above, $\lambda\bar X \sim

\mathsf{Gamma}(n,n)$ and R code qgamma(c(.025, .975), 100,100)/mean(y-20) returns the 95% CI $(0.015, 0.022),$ which contains $\lambda = 0.02.$

(b) You can search the Internet for the general case $(\lambda$ and $\theta$ both unknown) with key words '2-parameter exponential distribution' and 'shifted exponential distribution'. Estimation in the general case is of interest in

reliability theory and survival analysis. Web pages, lecture notes, and papers at various

degrees of sophistication are available, some of them behind credit card barriers.