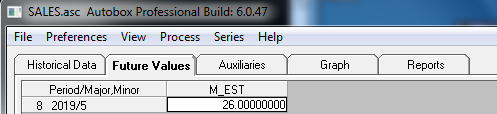

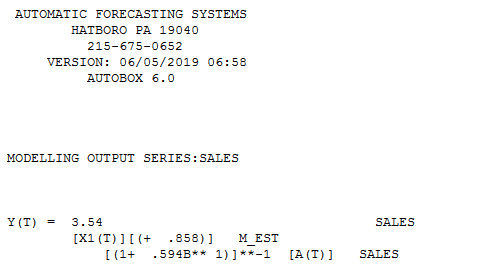

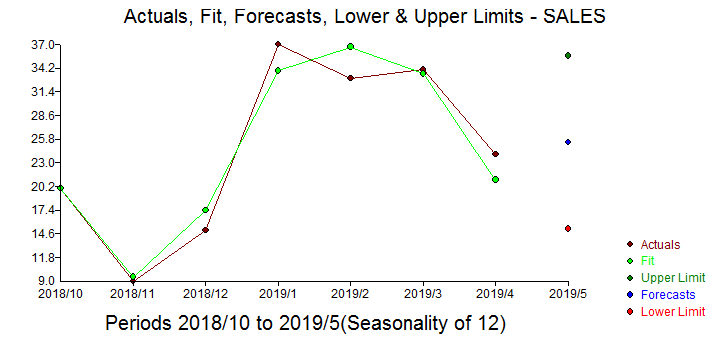

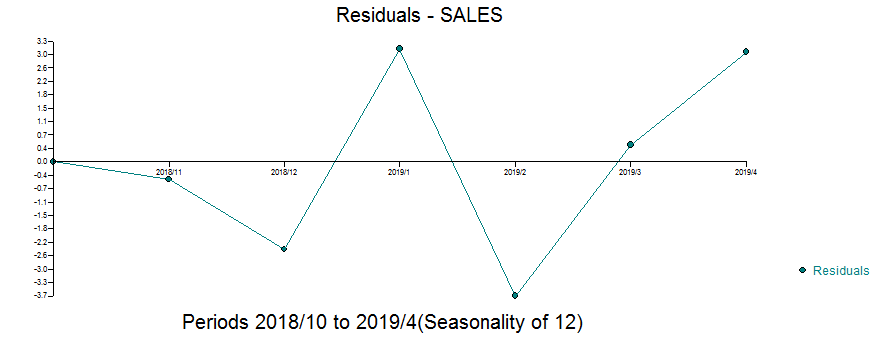

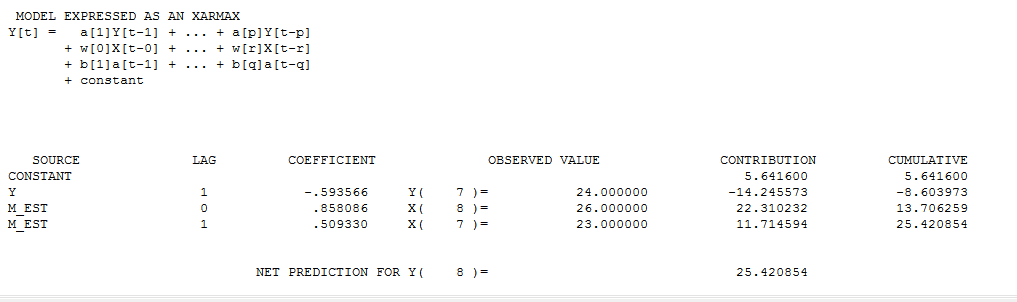

I have 3 stores differentiated by the StoreID, and I would like to predict the total sales across stores for the next month. I receive the Early Report of the sale as indicated by the ERSales column. This data comes in far ahead of the actual sales number. What I would like to do is predict an individual store's Sales for the next month based on their early report (the actual Sales and ER Sales are usually about the same as you can see by the UnitDiff column, but sometimes there is just bad bad or customer returns, etc.), and forecast a total sales number across all stores, which updates when I receive a new ERSales number for a store. Any suggestions or articles about how to approach the problem would be greatly appreciated.

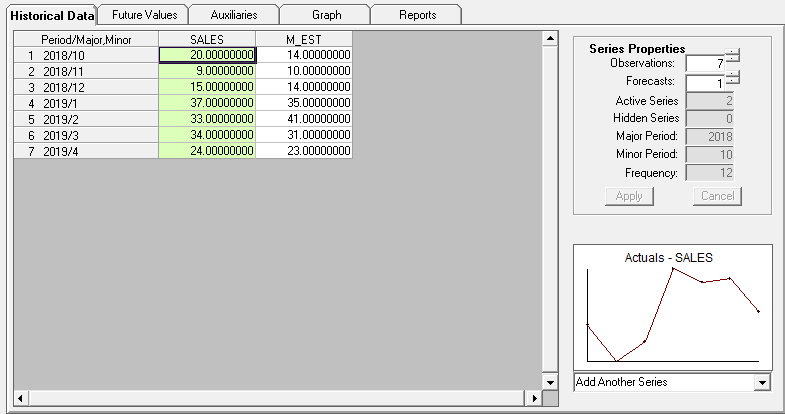

| Month | StoreID | Sales | 3MMAvg | ERSales | 3MMAvgER | UnitDiff | AvgDiff |

|-----------|---------|-------|--------|---------|----------|----------|---------|

| 10/1/2018 | 64 | 20 | 20.33 | 14 | 14.67 | 6 | 5.67 |

| 11/1/2018 | 64 | 9 | 15.00 | 10 | 12.67 | -1 | 2.33 |

| 12/1/2018 | 64 | 15 | 14.67 | 14 | 12.67 | 1 | 2.00 |

| 1/1/2019 | 64 | 37 | 20.33 | 35 | 19.67 | 2 | 0.67 |

| 2/1/2019 | 64 | 33 | 28.33 | 41 | 30.00 | -8 | -1.67 |

| 3/1/2019 | 64 | 34 | 34.67 | 31 | 35.67 | 3 | -1.00 |

| 4/1/2019 | 64 | 24 | 30.33 | 23 | 31.67 | 1 | -1.33 |

| 10/1/2018 | 143 | 19 | 29.67 | 20 | 29.00 | -1 | 0.67 |

| 11/1/2018 | 143 | 33 | 28.33 | 34 | 29.00 | -1 | -0.67 |

| 12/1/2018 | 143 | 11 | 21.00 | 12 | 22.00 | -1 | -1.00 |

| 1/1/2019 | 143 | 24 | 22.67 | 26 | 24.00 | -2 | -1.33 |

| 2/1/2019 | 143 | 22 | 19.00 | 24 | 20.67 | -2 | -1.67 |

| 3/1/2019 | 143 | 33 | 26.33 | 33 | 27.67 | 0 | -1.33 |

| 4/1/2019 | 143 | 29 | 28.00 | 28 | 28.33 | 1 | -0.33 |

| 10/1/2018 | 181 | 9 | 21.67 | 11 | 18.00 | -2 | 3.67 |

| 11/1/2018 | 181 | 18 | 16.00 | 13 | 12.33 | 5 | 3.67 |

| 12/1/2018 | 181 | 23 | 16.67 | 4 | 9.33 | 19 | 7.33 |

| 1/1/2019 | 181 | 5 | 15.33 | 9 | 8.67 | -4 | 6.67 |

| 2/1/2019 | 181 | 9 | 12.33 | 10 | 7.67 | -1 | 4.67 |

| 3/1/2019 | 181 | 10 | 8.00 | 17 | 12.00 | -7 | -4.00 |

| 4/1/2019 | 181 | 16 | 11.67 | 27 | 18.00 | -11 | -6.33 |