I hate to ask this question but I am going insane and other links haven't solved this problem. I have a seasonal ARIMA with just over two years of weekly data ARIMA(0,1,1)(0,1,1)[52]. It's highly seasonal and this model fits well enough for initial forecasting. I'm using Rob Hyndman's forecast package and the Arima and forecast functions within it. However, I am providing the forecasts and the forecasting equation to a client. So far, so good.

However, when I write out the forecasting equation I get numbers close but not equal to the forecast. I have double-checked my equation (here) and cannot figure out what I'm doing wrong. Here are the numbers:

Y_20_49 <- 791.7044 # One period back

Y_19_50 <- 516.0694 # One year ago

Y_19_49 <- 812.9433 # One year and one period ago

# Residuals acquired with sweep::augment();

# same as residuals(model)

resid_20_49 <- 1.048402e+01 # Residual one period ago

resid_19_50 <- -1.865834e+02 # Residual one year ago

resid_19_49 <- 2.784324e+01 # Residual one year and a period ago.

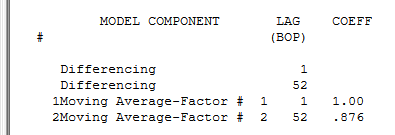

ma1 <- -0.8761 # MA1 coefficient from ARIMA

sma1 <- 1 # SMA1 coef from ARIMA

# Manual = 274.6686

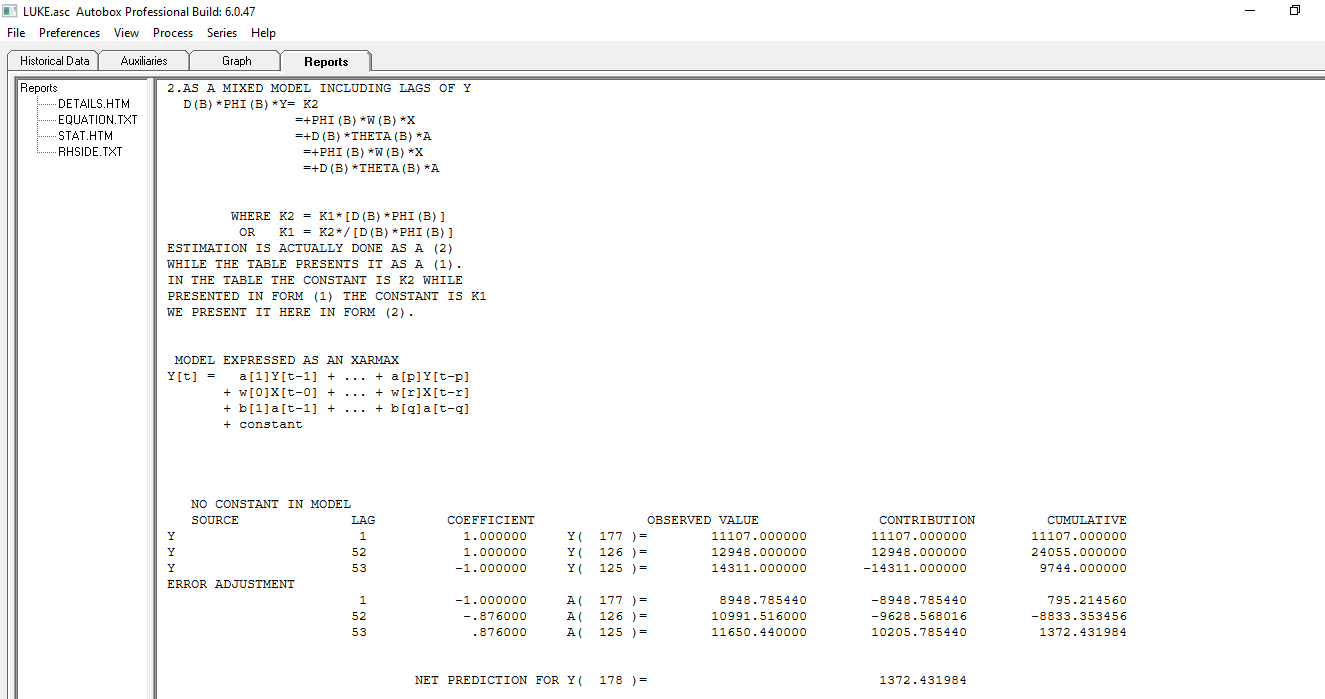

Manual <- Y_20_49 + Y_19_50 - Y_19_49 +

ma1 * resid_20_49 + sma1 * resid_19_50 +

(ma1 * sma1) * resid_19_49

Actual <- 334.4015 # Result from forecast(h = 1)

There's something obvious I'm missing but I'd appreciate any help. This model is not transformed but I have the same problem with another similar model that is logged.

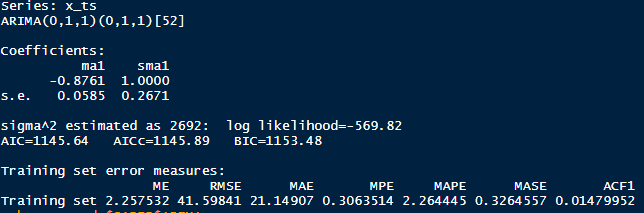

UPDATE: The model results report only MA and SMA terms; no constants. Here is a picture of the summary(model) results:

UPDATE2: The manual calculations seem to work when the MA and SMA terms are not close to one (even around abs(0.88) seems OK). I cannot be certain if this is the case but this happened during my quest to reproduce the forecasts.

forecastpackage result include a constant term? $\endgroup$