I'm struggling with testing the cointegration of 2 time series (or rather interpreting the test results properly).

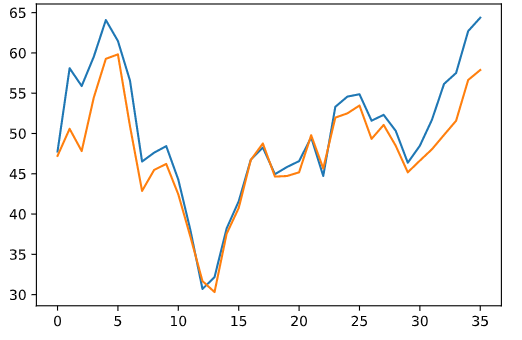

So I got 2 time series x and y each containing 36 monthly data points (oil prices).

From looking at those time series, I'd say they are cointegrated.

However when applying different cointegration tests, they don't seem to be:

1) Augmented Dickey-Fuller

from statsmodels.tsa.stattools import adfuller

from statsmodels.api import OLS

ols_result = OLS(y, x).fit()

result = adfuller(ols_result.resid)

returns

(0.6614451366946532,

0.9890361840444819,

10,

25,

{'1%': -3.7238633119999998, '5%': -2.98648896, '10%': -2.6328004},

84.12263429255607)

i.e. a p-value of 0.98; null hypothesis cannot be rejected, time series are not cointegrated.

2) Engle-Granger

coint_t, p_value, _ = coint(y, x)

p_value

0.06910078732250052

returns a p-value of 0.069 i.e. not cointegrated.

What am I doing wrong here?

Thanks in advance!

PS: there seems to be Granger-Causality between the 2 time series (tested using statsmodels.tsa.stattools.grangercausalitytests)

OLS_result.resid? $\endgroup$