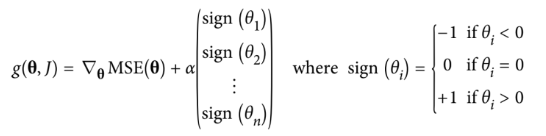

I'll give you hints towards the solution. We have your loss function $\mathcal L$:

$$\mathcal L(\boldsymbol\beta,\mathbf y,\mathbf X) = \frac{1}{2m}\sum_{i=1}^{m} (y_i - \beta_0 - \sum_{j=1}^{p}\beta_j X_{ji})^2 + \lambda\sum_{j=1}^{p}|\beta_j|$$

For context, gradient descent is a first-order optimization method for differentiable objectives.

Under gradient descent, we have:

$$\boldsymbol \beta_{n+1} := \boldsymbol \beta_{n} - \eta \nabla_\boldsymbol \beta \mathcal L$$

So we just need the gradient $\nabla_\boldsymbol \beta \mathcal L$ for every iteration.

That gradient is simply $\frac{\partial \mathcal L}{\partial \beta _k} \forall k \in [0,p]$.

For $\beta_k$ we can write generically:

$$\frac{\partial \mathcal L}{\partial \beta _k} = \frac{1}{2m}\sum_{i=1}^{m} \frac{\partial}{\partial \beta _k}(y_i - \beta_0 - \sum_{j=1}^{p}\beta_j X_{ji})^2 + \lambda \sum_{j=1}^{p}\frac{\partial}{\partial \beta _k}|\beta_j|$$

We can see that in the first term we have, using the chain rule:

$$\sum_{i=1}^{m} \frac{\partial}{\partial \beta _k}(y_i - \beta_0 - \sum_{j=1}^{p}\beta_j X_{ji})^2\\

=

\sum_{i=1}^{m} 2(y_i - \beta_0 - \sum_{j=1}^{p}\beta_j X_j)\frac{\partial}{\partial \beta _k}(y_i - \beta_0 - \sum_{j=1}^{p}\beta_j X_{ji})\\

=\begin{cases}

\begin{align}

&-\sum_{i=1}^{m} 2(y_i - \beta_0 - \sum_{j=1}^{p}\beta_j X_{ji}), &\text{if}\quad &k = 0\\

&-\sum_{i=1}^{m} 2(y_i - \beta_0 - \sum_{j=1}^{p}\beta_j X_{ji})X_{ki}, &\text{if}\quad &k \neq 0

\end{align}

\end{cases}

$$

The second term is easier to develop, since:

$$\sum_{j=1}^{p}\frac{\partial}{\partial \beta _k}|\beta_j|\\

=

\begin{cases}

0, &\text{if}\quad &k = 0\\

\frac{\partial |\beta_k|}{\partial \beta_k}, &\text{if}\quad &k \neq 0

\end{cases} $$