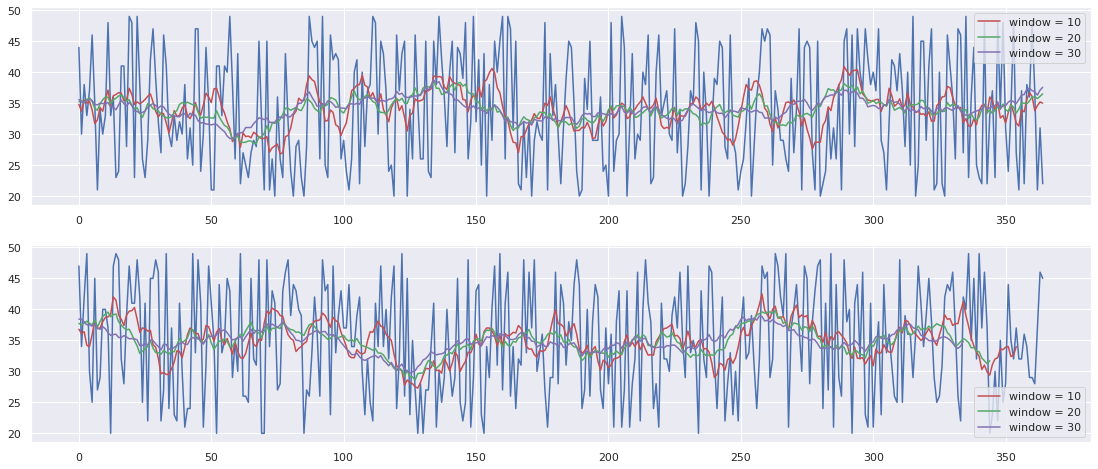

I am new to time series modelling and I was trying my hands on a dataset which records number of customers per day from 1 jan 2018 to 31 dec 2019. So far, I have tried implementing a naive moving average and got the following results.

Is this a legitimate fit? If this is not a right model, what approach should I use? Thanks

Things I have done:

- Checked data for stationarity: Data is stationary

- Implemented a moving average by calculating the average of previous 'window' number of observations as in the plot above.