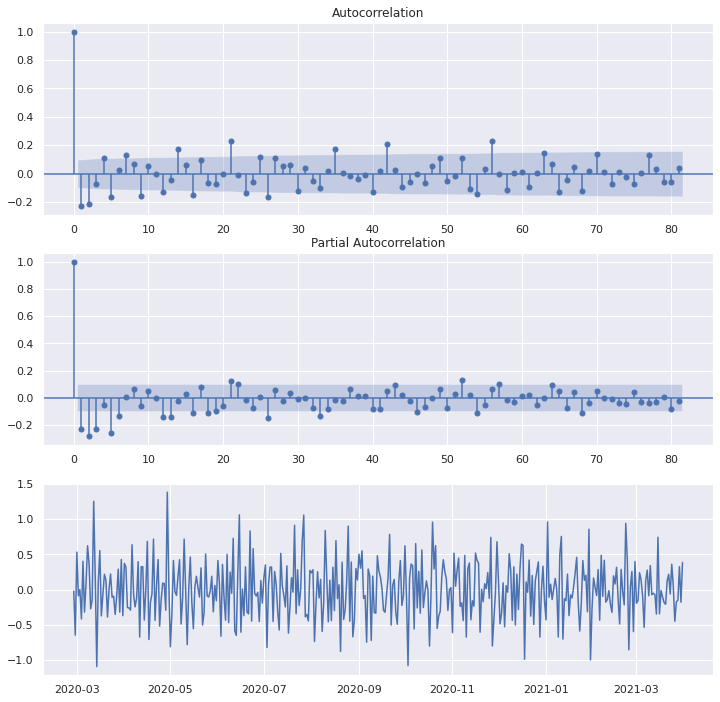

I'm a fairly new one to time series analysis. I was analyzing the daily trading volume of stock derivatives for the past year and trying to see if there is a seasonality pattern. I tried to make the time series stationary by doing a log transformation and shifting it by 7 days. I chose lags value by referring to this post. These are the plots I got after performing ACF and PACF, the plot on the bottom is the log-transformed volume shifted by one week.

However, I am confused by how should I interpret the results. Does it imply that there is a pattern occuring every 21 days? Or am I missing something while performing an analysis?

log_diff = fv['log'].diff()[7:]$\endgroup$