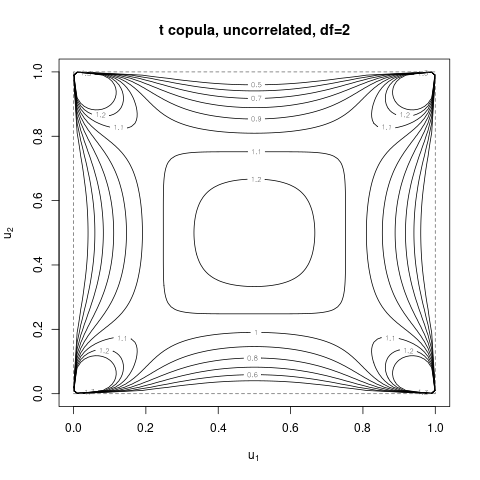

The uncorrelated $t$ copula is not the same as the independence copula. It is based on the multivariate $t$-distribution, which is an elliptical family, and the only elliptical distribution for which zero correlation implies independence is the normal. The difference can be quite large.

Below we will illustrate this using the R package copula. A contour plot of a $t$-copula is

The density of the independence copula is a constant 1. Note how the $t$-copula concentrates probability in the center and close the the four corners. The code used is

library(copula)

indCop <- ellipCopula(family="normal", param=0, dim=2, dispst="ex")

tCop <- ellipCopula(family="t", dim=2, dispst="ex", param=0, df=2)

getSigma(indCop)

[,1] [,2]

[1,] 1 0

[2,] 0 1

getSigma(tCop)

[,1] [,2]

[1,] 1 0

[2,] 0 1

# See they are different:

dCopula(c(0.5, 0.5), indCop)

[1] 1

dCopula(c(0.5, 0.5), tCop)

[1] 1.27324

contour(tCop, dCopula, n.grid=101, levels=c(0.5, 0.6, 0.7, 0.8, 0.9, 1, 1.1, 1.2, 1.3), main="t copula, uncorrelated, df=2")