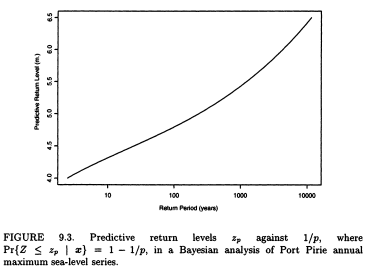

I was reading An Introduction to Statistical Modeling of Extreme Values by Stuart Coles, and I ran into a problem whilst trying to replicate a basic return level graph in R. For context, I first present the definition of a return level plot (p.49 of the book):

Estimates of extreme quantiles of the annual maximum distribution are then obtained by inverting Eq. (3.2): $$z_p = \begin{cases} \mu - \frac{\sigma}{\xi}\left[1-\{-\log(1-p)\}^{-\xi}\right], & \text{for } \ \xi \neq 0, \\ \mu-\sigma \log\{ -\log(1-p)\}, & \text{for } \ \xi =0,\end{cases} \tag{3.4}$$ where $G(z_p) = 1-p$. In common terminology, $z_p$ is the return level associated with the return period $1/p$, since to a reasonable degree of accuracy, the level $z_p$ is expected to be exceeded by the annual maximum in any particular year with probability $p$.

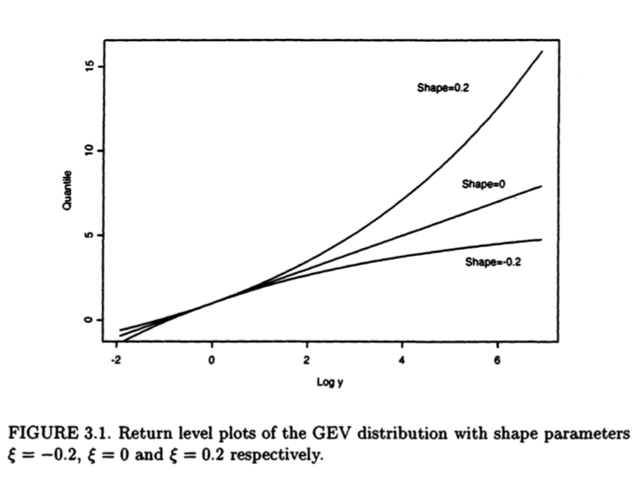

Since quantiles enable probability models to be expressed on the scale of data, the relationship of the GEV model to its parameters is most easily interpreted in terms of the quantile expressions (3.4). In particular, defining $y_p = -\log(1-p),$ so that $$z_p = \begin{cases} \mu - \frac{\sigma}{\xi}\left[1-y_p^{-\xi}\right], & \text{for } \ \xi \neq 0, \\ \mu-\sigma \log (y_p), & \text{for } \ \xi =0,\end{cases} $$ it follows that, if $z_p$ is plotted against $y_p$ on a logarithmic scale - or equivalently, if $z_p$ is plotted against $\log(y_p)$ - the plot is linear in the case $\xi = 0$.If $\xi < 0$ the plot is convex with asymptotic limit as $p \to 0$ at $\mu - \sigma/\xi$; if $\xi> 0$ the plot is concave and has no finite bound. This graph is a return level plot. Because of the simplicity of interpretation, and because the choice of scale compresses the tail of the distribution so that the effect of extrapolation is highlighted, return level plots are particularly convenient for both model presentation and validation. Fig 3.1 shows return level plots for a range of shape parameters.

As a reminder, $\mu,\xi \in \mathbb{R}$ and $\sigma > 0$ are the parameters of the GEV distribution. Now, I wanted to replicate Figure 3.1. To do this, I did the following:

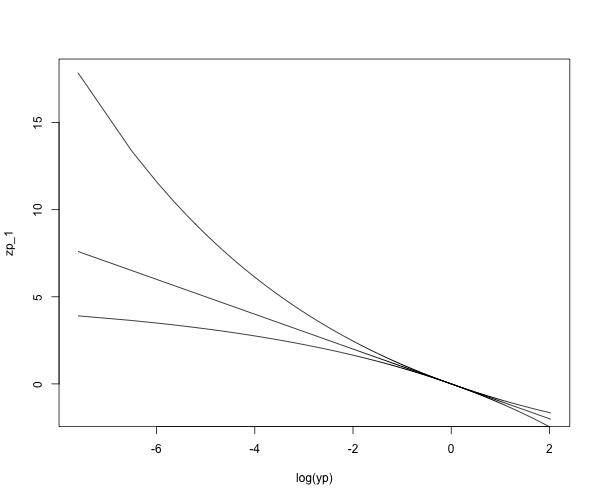

mu <- 0; sigma <- 1

p <- ppoints(1000)

yp <- -log(1-p)

zp_1 <- mu - (sigma/0.2)*(1-yp^(-0.2)) #xi = 0.2

zp_2 <- mu - sigma*log(yp) #xi = 0

zp_3 <- mu - (sigma/-0.2)*(1-yp^(0.2)) #xi = -0.2

plot(log(yp), zp_1, type = "l")

lines(log(yp), zp_2)

lines(log(yp), zp_3)

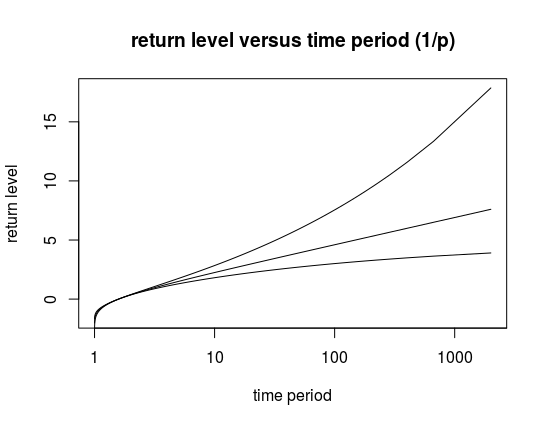

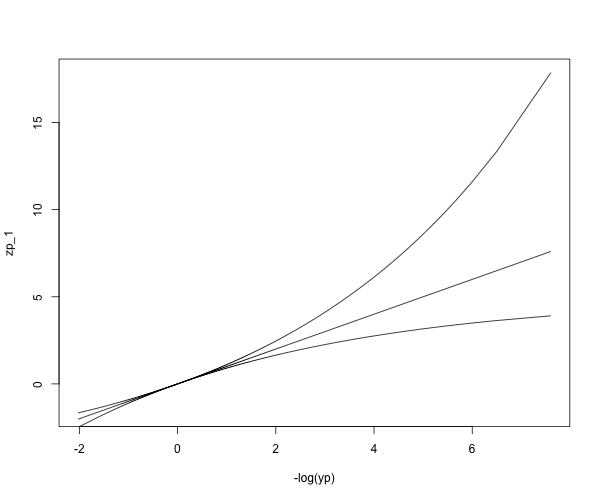

which produced the following plot:

Evidently, this plot is not the same as Figure 3.1. However, if instead of graphing $\{(\log(y_p), z_p), 0 <p<1\}$ we graph $\{(-\log(y_p), z_p), 0 <p<1\}$, we obtain the following:

plot(-log(yp), zp_1, type = "l")

lines(-log(yp), zp_2)

lines(-log(yp), zp_3)

which seems to be exactly Figure 3.1. I know the difference is just a sign, but is there something I am missing, theoretically? Did the author make a mistake? Any help is appreciated.