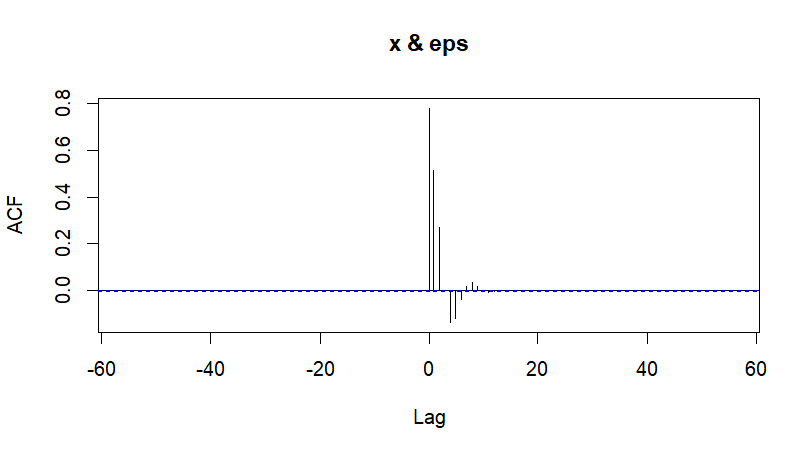

I know that an ARMA(p, q) refers to the model with p autoregressive terms and q moving-average terms. For example:

$$ X_t = c + \varepsilon_t + \sum_{i=1}^p \varphi_i X_{t-i} + \sum_{i=1}^q \theta_i \varepsilon_{t-i} $$

where $\varepsilon_{t} \sim WN(0,\sigma^2)$. That is, $E(\varepsilon_t) = 0$ and $E(\varepsilon_t \varepsilon_{t-j}) = 0$, for $j\neq 0$. Equivalently, $E(\varepsilon_t | \varepsilon_{t-j}) = 0$.

But in the books I've read, it doesn't tell me anything about the relationship between all the lags of $\varepsilon_t$ and all the lags of $X_t$. For example:

- Are $X_t$ and $\varepsilon_t$ independent? And how about $X_t$ and $\varepsilon_{t-j}$?

- If not, are they mean independent? That is: $E[X_t | \varepsilon_{t-j}] = X_t$?

- Are they not correlated? That is, $cov(X_t,\varepsilon_{t-j})=0$?

Some help?