I'm looking at Norwegian export data to try to detect sanctions evasion by Russia. Sanctions evasion takes place by the export of goods to third-party countries that in turn re-export the goods to Russia. The data have a monthly resolution, and they are highly granular in terms of categories of goods. I want to know whether there is a statistical test I can use that can detect significant changes in exports after February 2022 compared to before. I would like to use that test to check each individual export category for a number of third-party countries in order to know what to take a closer look at.

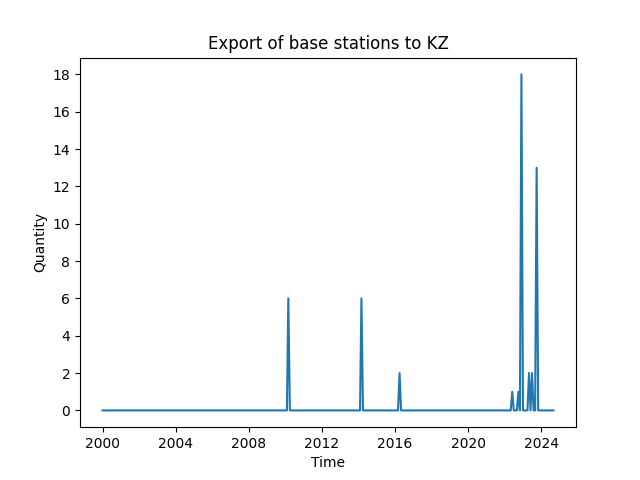

Below I've plotted a time series of exports of base stations (telecom equipment) to Kazakhstan:

This is a typical example of what the data in the dataset looks like. You can see that most of the monthly values are zero, with a few non-zero values. The values are discrete, with only whole numbers.