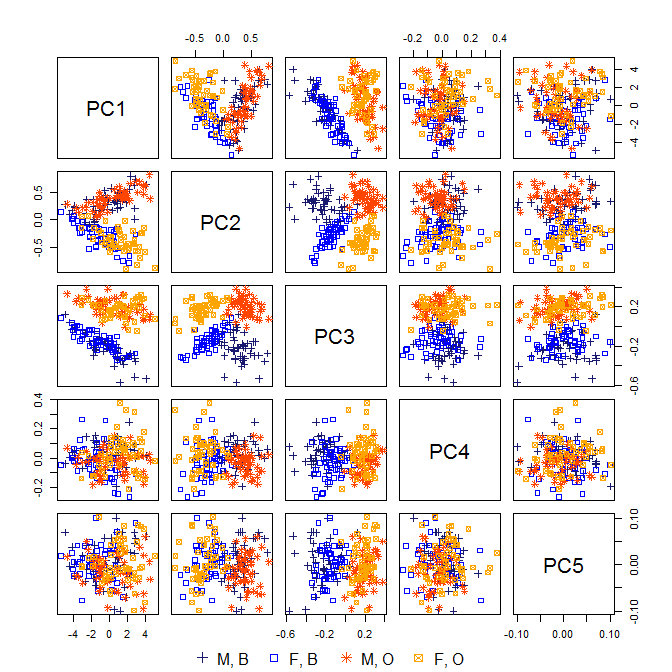

I have noticed that PCs with low variance are most helpful when performing a PCA on a covariance matrix where the underlying data are clustered or grouped in some way. If one of the groups has a substantially lower average variance than the other groups, then the smallest PCs would be dominated by that group. However, you might have some reason to not want to throw away the results from that group.

In finance, stock returns have about 15-25% annual standard deviation. Changes in bond yields are historically much lower standard deviation. If you perform PCA on the covariance matrix of stock returns and changes in bond yields, then the top PCs will all reflect variance of the stocks and the smallest ones will reflect the variances of the bonds. If you throw away the PCs that explain the bonds, then you might be in for some trouble. For instance, the bonds might have very different distributional characteristics than stocks (thinner tails, different time-varying variance properties, different mean reversion, cointegration, etc). These might be very important to model, depending on the circumstances.

If you perform PCA on the correlation matrix, then you might see more of the PCs explaining bonds near the top.