Imagine that you have $1000 that you can split however you want. You bet in a cockroach run, but it is not the finish that's interesting. You can bet for the cockroach to go left or right, and you gain proportionally to how much he moved in or against your favour from the time you enter to the moment you decide to quit.

But you're smart. You have found that there are patterns, and our little hero tends to reach some areas with some probability before finally turning around and going in the other direction.

By the final turn, we mean that in his infinite race, he will not drift further to the left or right for the next 24h. He will either stick to the side or drift to the other side where the second is much more probable.

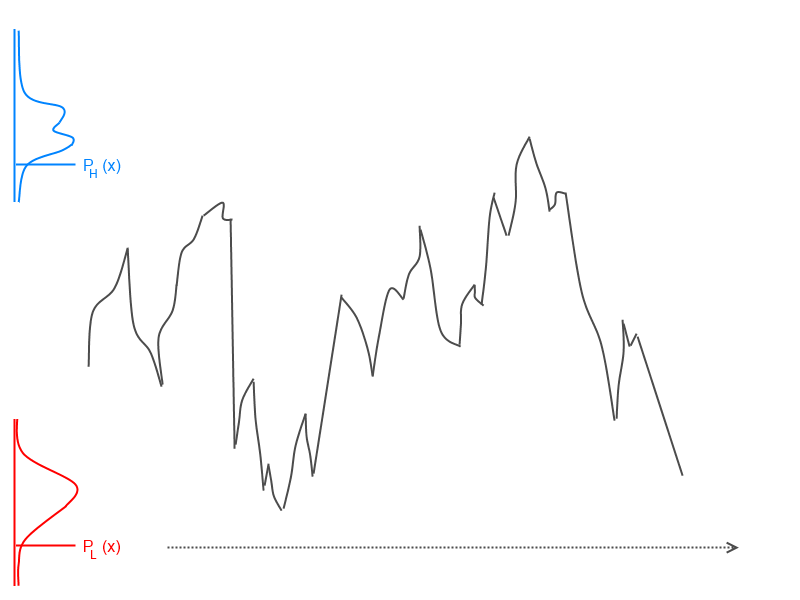

The blue and red histograms (normalized to 1.0) show the probability of the furthest positions that the cockroach reaches before he turns around (makes the final turn before he begins his long journey to reach the other side).

The black lines show the path of the cockroach.

From the histograms that show the statistically collected histogram of the extreme turning point, you can easily calculate the expected values for most extreme drift to the left or to the right.

You get paid 1 dollar for each millimeter that the cockroach rifts in your favour, and you lose 1 dollar when he goes 1 mm against you.

You decide when to enter and when to exit to collect gain or loss.

There are a few interesting optimization questions:

There are a few interesting optimization questions:

How should you enter your partial bets to enter for as close to $1000 as possible and to get as close to expected value as possible (I think that exceeding it is not possible)?

How should you proceed with quitting all you have managed to enter (probably you have not managed to enter with whole $1000)?

How to deal with misses? As far as missing enters is not a big deal, missing an exit point might lead to a complete disaster because the 'little puppy' is not going against you.

Should we need to measure some other properties of the path to make better bets as for the 'averaging' of entry / exit positions?

These questions puzzle me a lot, and finding a clue toward solving at least one will let me sleep better. :)