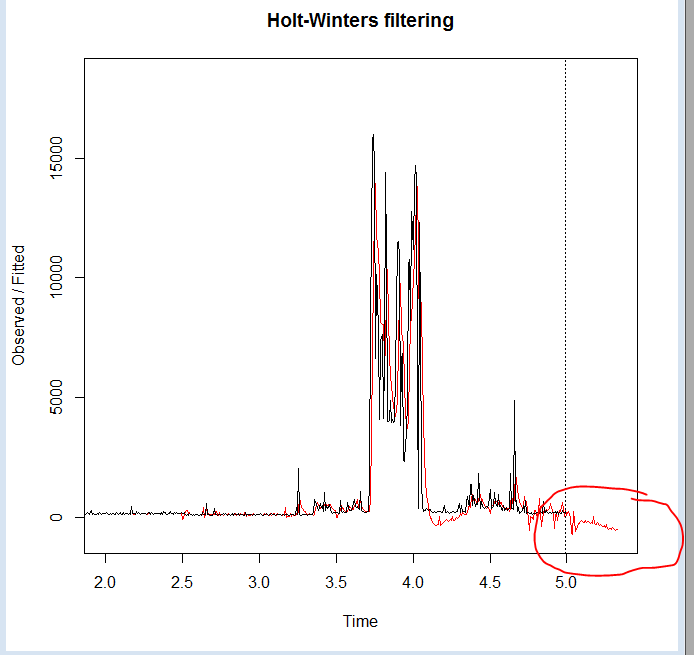

I understood that Holt Winters forecasting may results in negative values due to trending. I did reduce trending component value, but still forecast values are negative territory. Our data set will never be in negative values (like electricity data set, which never falls below ZERO).

What sort of post algorithm techniques we can apply to make this value as non-negative value? Any help would be appreciated.

This implementation is in Java, so I can't use ets() package at this point of time (and I am assuming ets() also can't avoid negative values).