I would appreciate if someone could check the mathematical equation for the seasonal ARIMA (4,1,4) x (1,1,1) period 12 that I wrote. I have done it this way, but I am not really sure if it correct is. Can someone check it and correct it? I would be graetfull.

$(1+0.0789359 B - 0.0007957 B^2- 0.7559195B^3 + 0.2814265B^4)(1+0.0851737 B^{12}) (1-B) (1-B^{12}) Y_t= (1 - 0.4212575 B - 0.2042966 B^2 -0.9272988 B^3 + 0.5528213B^4)(1-0.8477401B^{12})e_t$

Please just tell me if I am thinking right. Coefficients here:

Thank you for your answer!

but how can I simplify it?

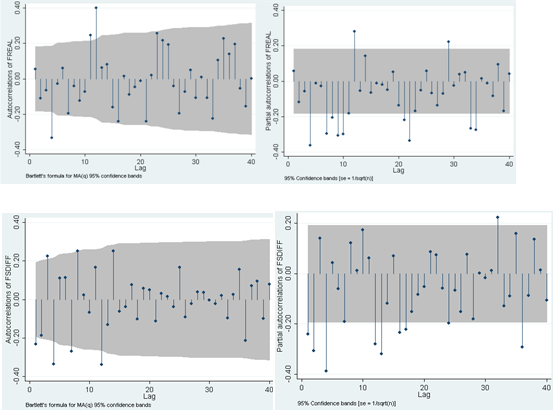

I am very new to SARIMA and I am really facing a poblem which p,q,P,Q to use. Here is ACF and PACF of first-difference (two top plots), and ACF and PACF of first-seasonal difference.

I think that P=1, Q=1 because ACF and PACF of first-seasonal difference drop off at lag 1 and are outside the confidence band. What about p and q ? Can I then say that p=2 and q=2 because it drop of at lag 2? Or should I take under consideration the fact that only at lag 4 ACF and PACF are outside confidence band? Is p=4 and q=4 or 2 for both?

Or should I do AIC test for (2,1,2)(1,1,1)12, (4,1,2)(1,1,1)12, (2,1,4)(1,1,1)12, (4,1,4)(1,1,1)12 and check which one has the smallest? Or assuming that p=2 and q=2 does not make any sense because its within the confidence band?