I would appreciate if someone could check the mathematical equation for the seasonal ARIMA (4,1,3) x (1,1,1) period 12 that I wrote. I have done it this way, but I am not really sure if it correct is. Can someone check it and correct it? I would be graetfull.

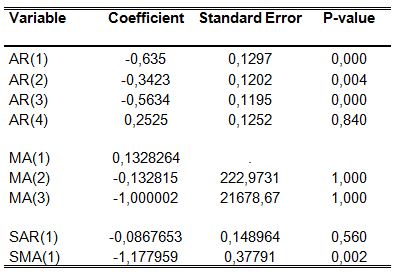

$(1+0,6350877 B + 0.342846B^2 - 0.5634599B^3 - 0.0252533B^4)(1+0.0867653 B^{12}) (1-B) (1-B^{12}) YT= (1 + 0.1328264 B - 0.132815 B^2 – 1.000002 B^3)(1-1.177959 B^{12})E_t$

Should I drop non-significant coefficients and leave it this way? $(1+0,6350877 B + 0.342846B^2 - 0.5634599B^3)(1-B) (1-B^{12}) Y_t=(1-1.177959 B^{12})E_t$

Here are my results:

Which formula will be better? Thank you in advance. Kind regards